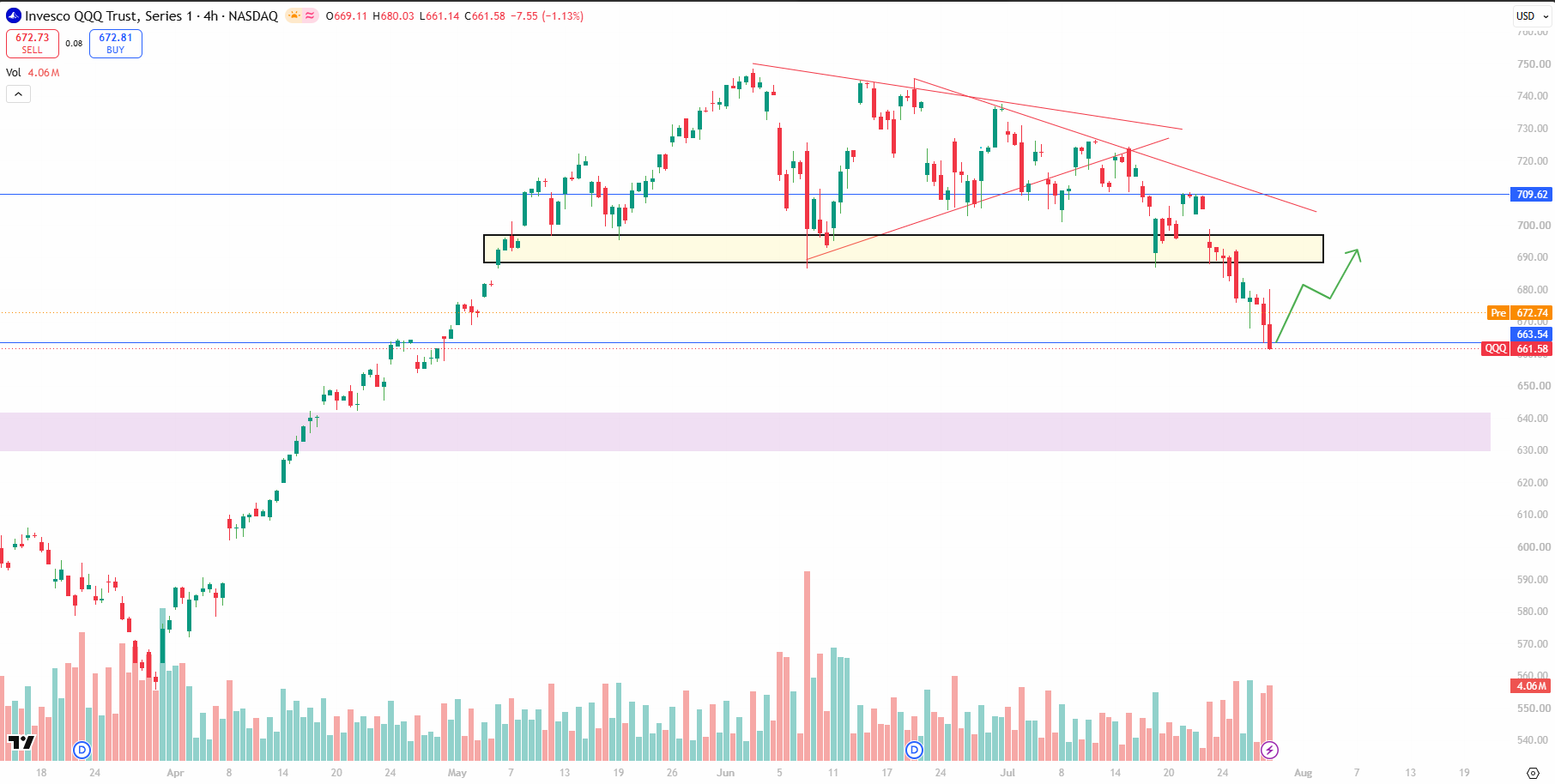

- Key support holding: QQQ has rebounded strongly from the 663-665 support zone, showing buyers are defending this level after the recent sharp selloff.

- Retesting previous support: Price is now testing the 688-695 supply/resistance area (highlighted box), which previously acted as support and has now flipped into resistance.

- Breakout confirmation: A sustained close above 695 would invalidate the recent breakdown and open the door for a move toward 709-710, with the descending trendline becoming the next major hurdle around 715-720.

- Resistance still intact: Until QQQ reclaims 695, the short-term trend remains cautious as lower highs continue to respect the descending trendline.

- Bearish rejection scenario: If price gets rejected from the 695 zone, sellers could push QQQ back toward 680, followed by a retest of the 663 support.

- Bias: The recent bounce is encouraging, but 695 remains the key decision level. A breakout favors continuation higher, while rejection keeps the broader corrective structure intact.

J

NASDAQ (QQQ) 4H: Break Above 695 Could Trigger Rally to 710+

A

EARNING WEEK AHEAD

J

TESLA ~ A Clean Setup on the Chart. Sitting on a Line It Has Defended for Five Years

TSLA (Tesla, Inc.) — Price $311.21 | Mkt cap ~$1.22T

Record revenue, collapsed profit, and a stock resting on the exact level that has decided its last five years.

OVERVIEW

- Trades at $311, down ~38% from the ~$498 high (Dec 2025).

- Q2 2026: record revenue, big profit miss — stock fell ~17% after the print.

- BYD retook the global BEV crown (557k vs Tesla's 480k in Q2).

- US $7,500 EV credit expired Sep 2025; European brand backlash persists.

- Story has shifted from carmaker to "physical AI" — robotaxi, FSD, Optimus.

BUSINESS MODEL

- Automotive ~73% of revenue, Energy ~11%, Services ~16%.

- Direct-to-consumer sales, no dealer network.

- FSD is the margin lever: 1.48M subscriptions, +56% YoY.

- Regulatory credits collapsed to $146M from $439M — that free profit is gone.

- Four gigafactories: Fremont, Shanghai, Berlin, Austin.

FUNDAMENTALS

- Q2 revenue $28.24B, +26% YoY — first TTM above $100B.

- Operating income $398M, down 57%; operating margin just 1.4%.

- Non-GAAP EPS $0.33 vs ~$0.50 expected.

- Free cash flow negative $1.09B — capex $5.79B, first negative quarter since 2024.

- Cash $43.5B; deliveries 480k (+25%); energy storage 13.5 GWh (+41%).

VALUATION

- Forward P/E ~165. Trailing ~288. PEG ~5.6.

- Toyota trades at ~9x, GM ~6x, Ford ~9x forward.

- Even NVDA (19x fwd) and AAPL (34x fwd) are a fraction of this.

- Price/sales ~12x vs ~0.3x for GM and Ford.

- Analyst average target ~$399 (range $125–$600), consensus split Buy/Hold.

TECHNICAL ANALYSIS (weekly chart)

- Price sitting on confluence: the 300–320 multi-year box and the rising trendline from the 2024 low.

- That 300–320 zone was resistance for years, now support — classic polarity level.

- Red descending trendline from the $498 high caps rallies around 355–360.

- Weekly close below 285 breaks both structures → opens 260, then 230.

- Weekly close above 370 and through the trendline flips it bullish.

- Setup on chart: long 311, target 370, stop 285 → ~2.3:1 R:R.

GROWTH OUTLOOK

- Robotaxi live in Austin, Miami, Orlando, Tampa; Cybercab consumer sales targeted 2027.

- FSD v15 expected H2 2026 — though timelines have slipped repeatedly.

- Optimus V3 production starting, but Musk himself called the ramp "quite slow."

- Energy is the quiet winner: Megapack 3 and Megablock ramping through 2026.

- Capex above $25B this year, plus a debt facility up to $30B being arranged.

- Risks: margin compression, China share loss, tariffs, autonomy delays, key-person risk.

BOTTOM LINE

- Volumes recovered, but profitability collapsed to fund the AI build-out.

- Bull case: autonomy and Optimus convert Tesla into a high-margin AI platform.

- Bear case: a margin-compressing automaker losing share, valued at 165x forward earnings.

- Level to watch: 285 on the downside, 370 on the upside. Everything between is noise.

- Research only, not investment advice.

J

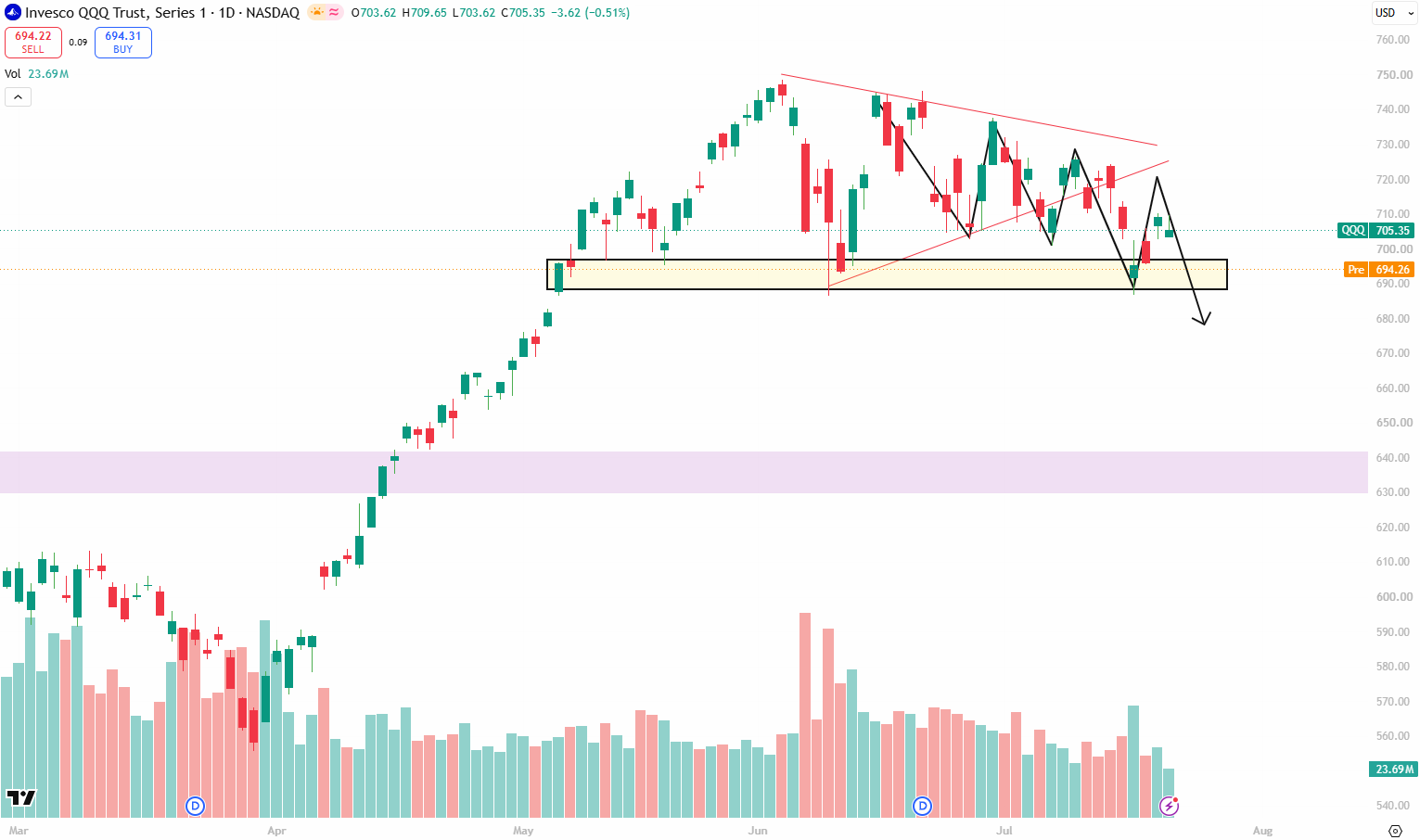

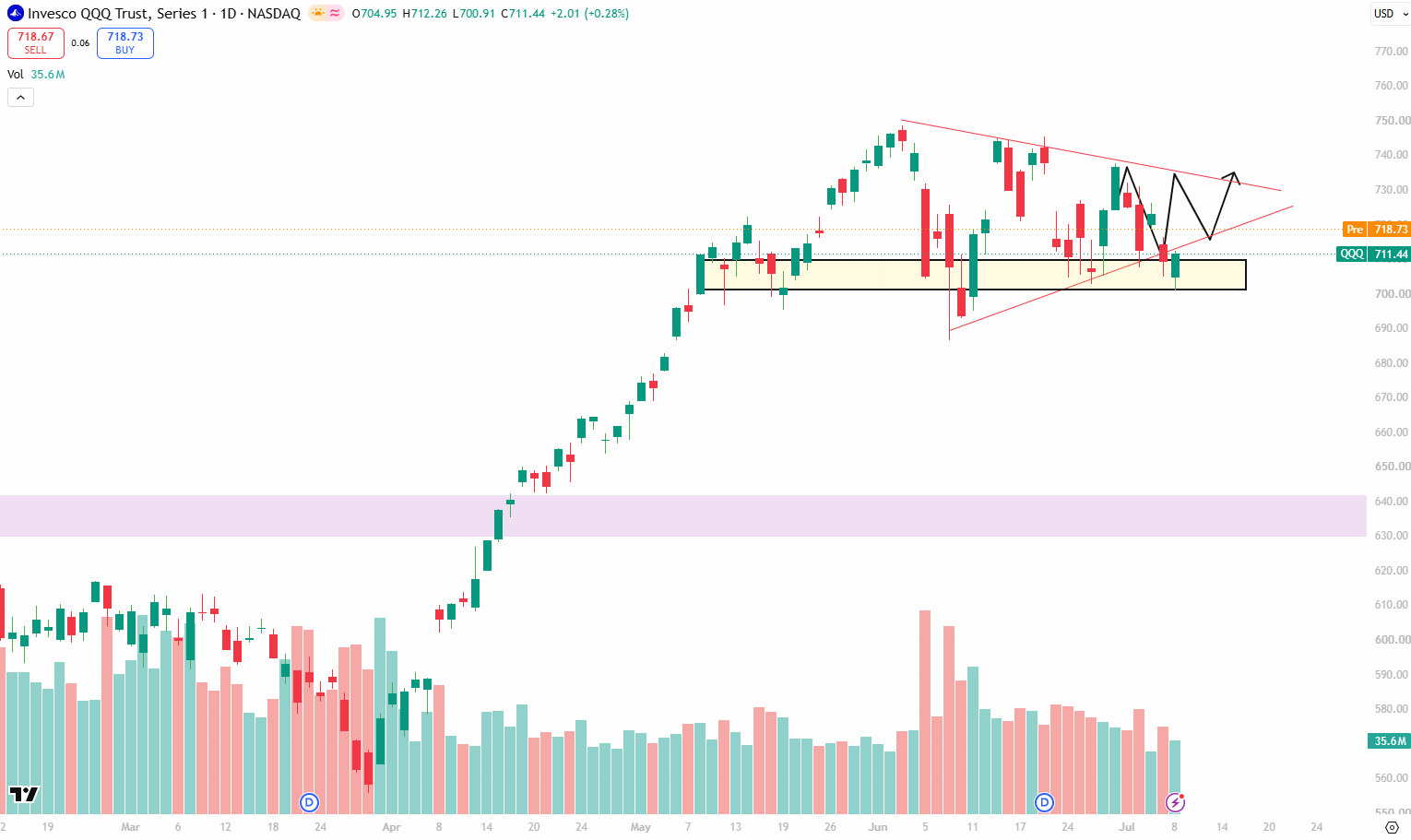

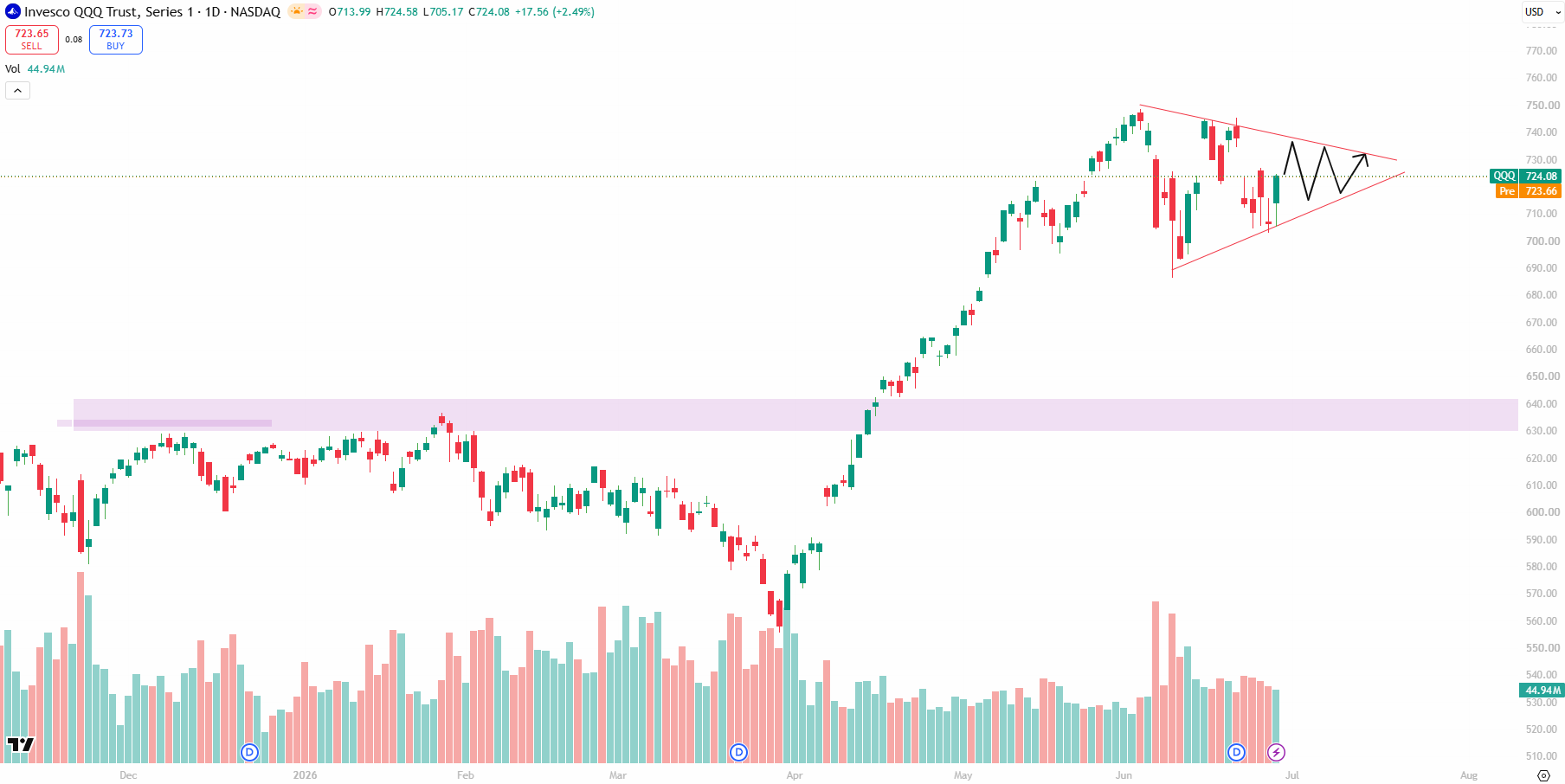

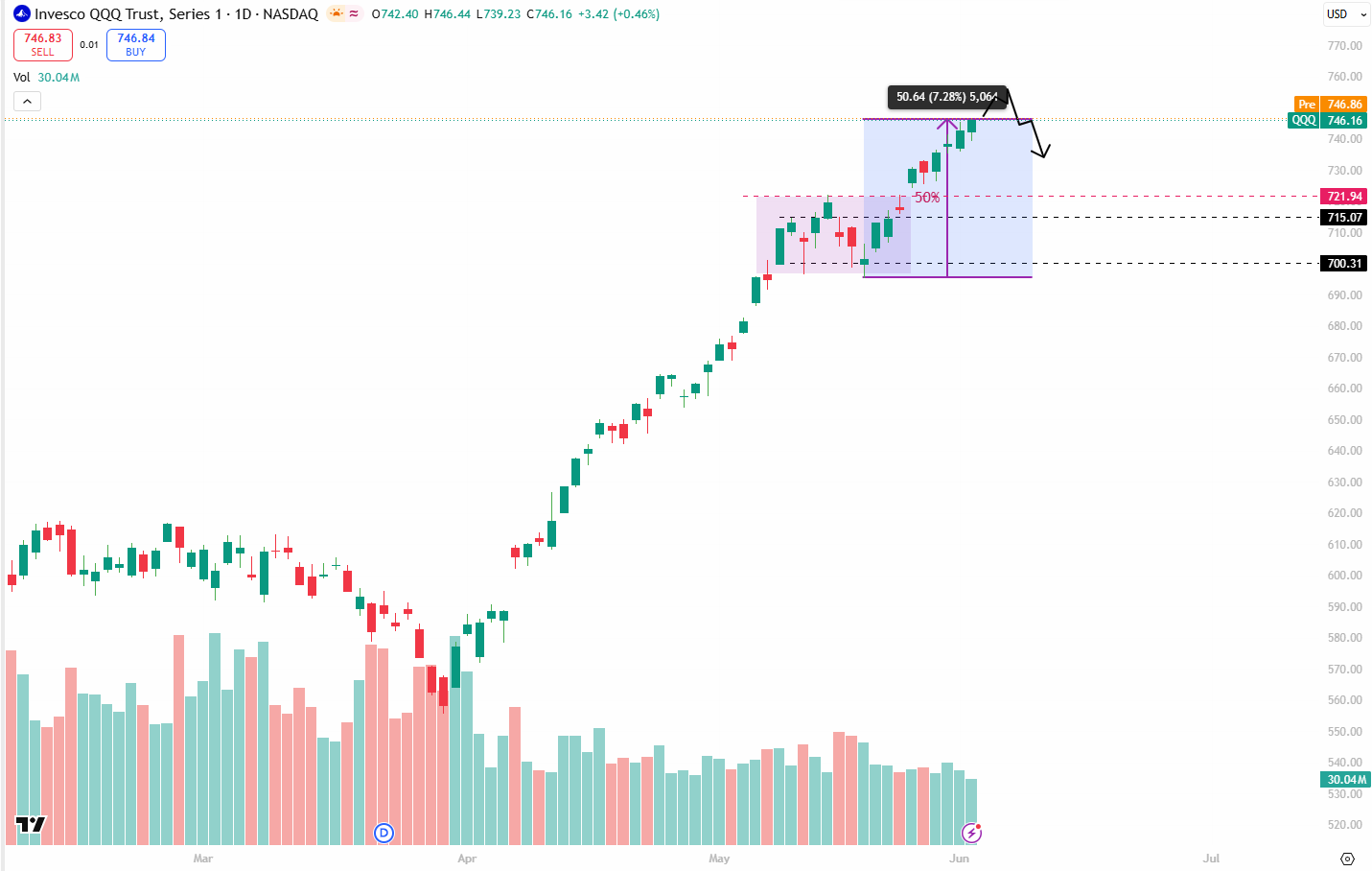

NASDAQ (QQQ) Price Action: Decision Zone Could Shape the Next Move

- Strong pullback from the 663 support is now testing the 695 resistance, the last major supply zone.

- A daily close above 695 could extend the rally toward the 715–720 descending trendline resistance.

- A rejection from 695 may signal the continuation of the bearish trend, with 640 as the next major support.

- The 689–695 (yellow box) is the key decision zone that will likely determine the next directional move.

- Price action: The current rally looks like a pullback within a downtrend until key resistance is reclaimed.

- Overall outlook: The short-term trend remains bearish while price trades below the falling trendline; this is the pullback phase of a downtrend move.

J

QQQ Tests Major Demand Zone After Sharp Sell-Off. Here's What Comes Next

- Bearish Breakdown Confirmed: QQQ has decisively broken below the 690–695 demand zone, confirming a loss of bullish momentum. Price is now trading near the 660 support level, which is the next major technical area to watch.

- 660 Level Achieved as Expected: As highlighted in our earlier update, we expected QQQ to decline toward the 660 level before a meaningful bounce could develop. Price has now reached that target, making this a critical reaction zone for buyers.

- Key Resistance Levels: Any recovery is likely to face initial resistance at 690–695 (previous support turned resistance), followed by 710, with stronger resistance in the 725–730 region where the descending trendline is located.

- Important Support Levels: Immediate support is around 660–663. A failure to hold this area could trigger another leg lower toward the 630–635 demand zone, which is the next major higher-timeframe support.

- Expected Move: As long as 660 holds, a relief rally toward 680–695 is the higher-probability scenario. However, the broader trend remains bearish, so any bounce should be viewed as a recovery unless QQQ reclaims 695–710 with strong buying volume.

J

Entendicare Inc (old age care industry)

I am buying this stock few every month. What is your view. Old age Care industry:

What you think?

J

BE at the Line That Never Broke 4th Touch, Revenue Up 130%, Stock Down 53%.

Bloom Energy (BE) at the Line That Never Broke 4th Touch, Revenue Up 130%, Stock Down 53%.

Chart Says Decision Point.

Business

- Makes fuel cell "boxes" that generate power on-site, no grid needed.

- Sells the box once + 10–15 year service contracts after.

- Buyers = AI data centers stuck in 4–7 year grid queues. Oracle & Brookfield are the big names.

Technicals

- ~$163–169, down ~53% from the $351 June peak.

- Sitting exactly where the July-2025 rising trendline meets the $168–185 old resistance box — 4th touch, real confluence.

- But below the 20/50/200 DMA but still trading at a very strong support area from where there is a very high chance of trend reversal.

- Hold $157 = setup alive. Lose it → $120–125 next.

- Upside: $185–190 → $230 → $270.

Fundamentals

- Q1 rev +130% to $751M, first real operating profit ($72M), $2.5B cash. Growth is genuine.

- FY26 guide: $3.4–3.8B revenue, EPS $1.85–2.25.

- The problem: claims a "$20B backlog," but audited filings show ~$492M. Short sellers are attacking this.

- Also: China scandium sourcing allegations, Oracle's Jupiter pipeline rejected twice, heavy Brookfield concentration.

- Still ~82x forward earnings.

⚡ Snapshot

| Price | $163–169 |

| From peak | −53% |

| YTD | still +116% |

| Trend | Broken — below all key MAs |

| Support | $157–169 (trendline + box) → $120–125 |

| Resistance | $185–190 → $230 → $270 |

| Story | Real revenue growth vs. real credibility questions |

G

TSM Head & Shoulders Breakdown Setup

Taiwan Semiconductor ($TSM) is testing the neckline of a clean head-and-shoulders top — and a confirmed break opens the door to $291.50.

The Pattern

Left Shoulder: ~$415–$420 (early May)

Head: ~$483–$485 (mid-June, 50%+ rally from March)

Right Shoulder: ~$430–$432 (mid-July)

Neckline: Flat at ~$388–$390

The Test Regular session closed at $399.09 — above the neckline. Pre-market is already printing $384.20, below it.

What Confirms It A daily close below ~$388–$390 with follow-through the next session. Pre-market alone doesn't count. The close is what matters.

The Target Pattern height: ~$95 ($484 head – $389 neckline). Projected down from the neckline = $291.50. That level also happens to sit right at the March 2026 base — giving it independent structural support.

Bottom line: Watch the close. A confirmed neckline break puts $291.50 in play.

J

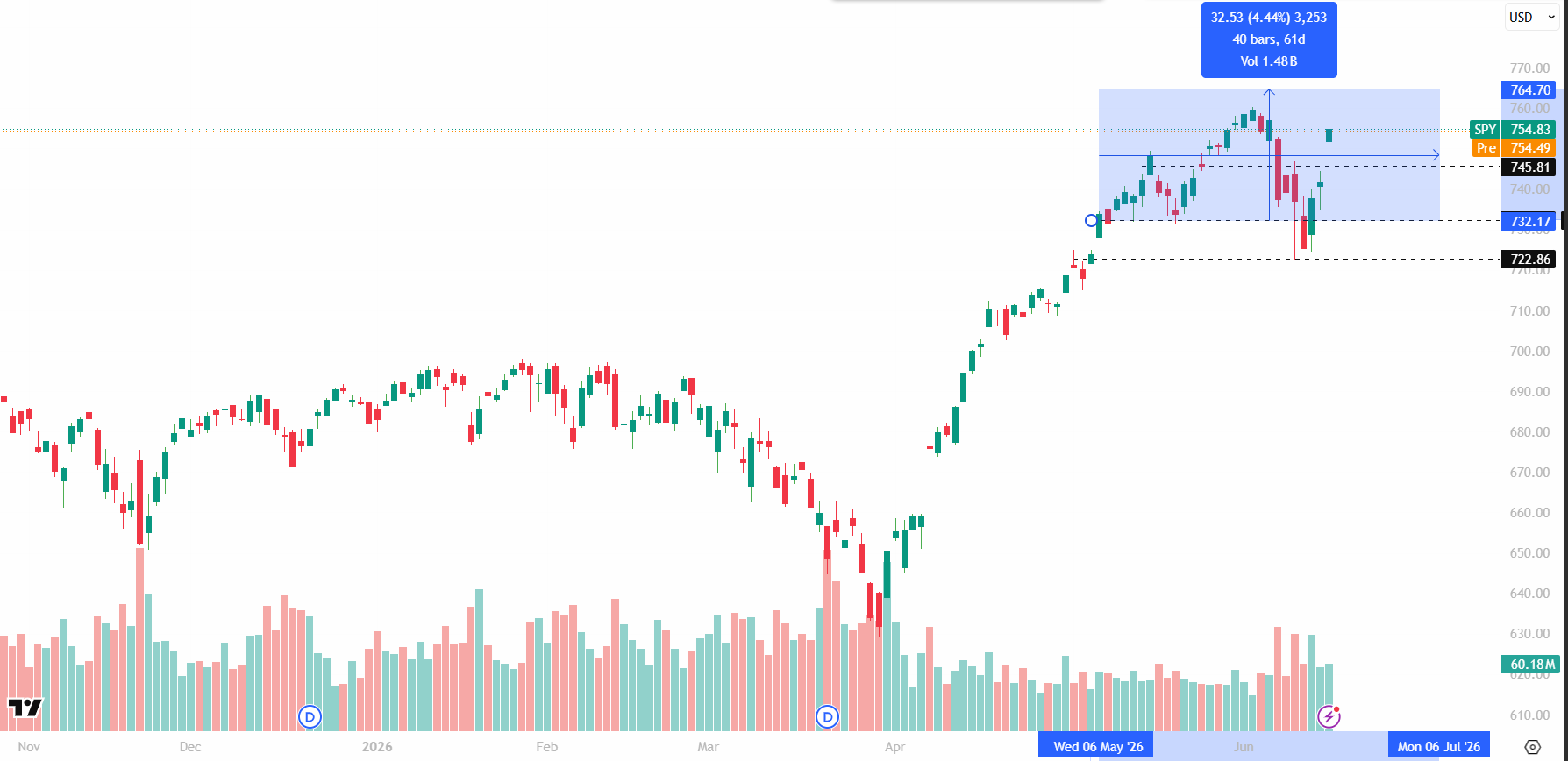

SPY Set for High-Volatility Move as Triangle Tightens.

- SPY continues to trade inside a tightening symmetrical triangle, with support near 732.60 and immediate resistance at 755.50, indicating a major breakout is approaching.

- A decisive daily close above 755.50 would confirm a bullish breakout, opening the door for a retest of 760.20, with the potential for further upside if buying momentum accelerates.

- Failure to hold the rising trendline could trigger a short-term pullback toward the 732.60 support zone, where buyers are expected to defend the broader uptrend.

- A confirmed breakdown below 732.60 would invalidate the current bullish structure and increase the probability of a deeper correction toward the 710–715 region.

- Price remains compressed between rising support and descending resistance, suggesting volatility is likely to expand sharply once either side of the pattern is broken.

- Key Levels to Watch: Resistance: 755.50 → 760.20 | Support: 732.60 → 710–715. Wait for a confirmed breakout or breakdown before taking directional positions to avoid false moves.

J

NASDAQ: Pre-Market Bounce or Bear Trap? QQQ Tests Key Support

- QQQ has broken below the major support zone at 688–694, signaling increasing bearish momentum. A daily close below this area would confirm the breakdown and favor further downside.

- The NASDAQ continues to trade below a descending trendline, keeping the short-term trend bearish. Until this trendline is broken, rallies are likely to be viewed as selling opportunities.

- Today's pre-market level around 694 is the key opening price to watch. If QQQ opens above 694 and holds that level after the opening bell, buyers could attempt a recovery toward 700–705. A gap-up with strong volume would improve the bullish outlook.

- If the pre-market gains fade and QQQ opens or slips back below 688–690, it would reinforce the bearish breakdown and could trigger another wave of selling.

- A sustained move above 700–705 would be the first sign that bulls are regaining control, with the next resistance coming near 715–720 and the descending trendline.

- Failure to reclaim the 688–694 support zone keeps the downside risk intact, with the next major support area located around 630–635, which remains the next significant demand zone on the daily chart.

J

QQQ Technical Analysis: All Eyes on the 688–700 Range

- QQQ continues to respect the major support zone around 688–690, where buyers have stepped in multiple times. This remains the key level to watch.

- A break above yesterday's high (~700) could trigger fresh bullish momentum, opening the door for a move toward the 710 resistance zone.

- The descending trendline overhead remains the primary resistance, and a confirmed breakout above it is needed to shift the short-term trend back to bullish.

- A sustained close below 688 would weaken the current market structure and increase the probability of a deeper downside move.

- Today's key trading range is 688–700. Price action within this zone is likely to remain choppy until a decisive breakout or breakdown occurs.

- This week's closing price could determine next week's direction. A close above resistance would favor bullish continuation, while a close below support would strengthen the bearish outlook—assuming no major unexpected news changes market sentiment.

J

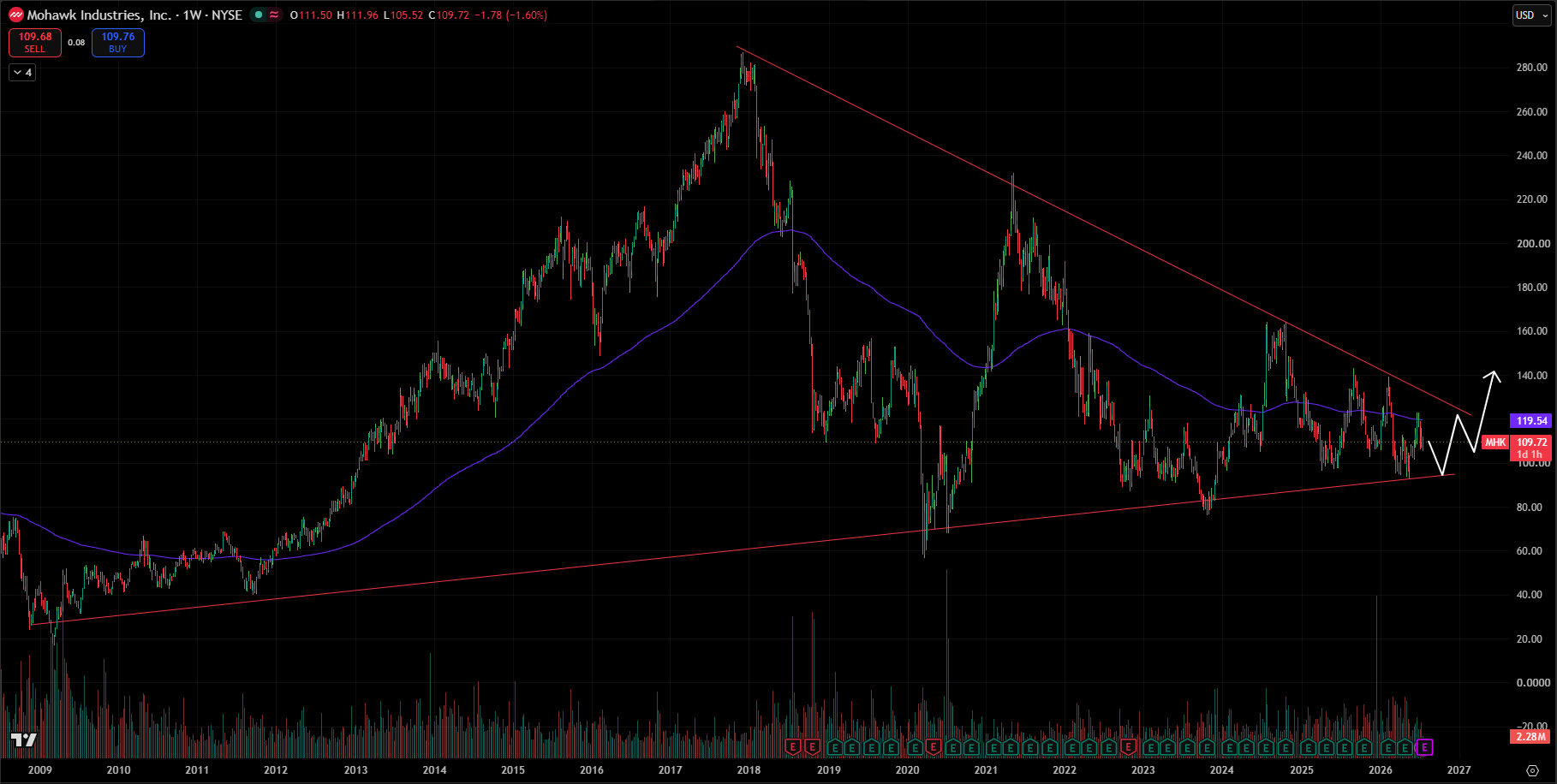

MHK: Mohawk, An 8-Year Pattern Meets a July 30 Earnings Print. Coils Into an 8-Year Apex.

Technical Chat Setup with Value — Mohawk Industries (MHK): Eight-Year Coil Nearing Resolution

Weekly chart | NYSE | Price: $109.65

The setup

- MHK has been compressing since 2018 and is now in the final few percent of the range.

- Upper boundary: a falling trendline anchored at the December 2017 all-time high near $285, connecting the 2021 high near $232 and every lower high since.

- Lower boundary: a rising trendline climbing since the 2009 low near $28, with touches in 2012, 2020 and 2024.

- Volume has been contracting into the apex — typical behaviour before a range resolves.

Resistance — what confirms

- The falling trendline sits near $120 today.

- The long-term weekly moving average sits at $119.54 — effectively the same level.

- That confluence is why every rally since 2024 has stalled just underneath it.

- A weekly close above $120 would be the first close above the line in eight years, and is the confirmation trigger.

Support — what invalidates

- The rising trendline sits near $93, last tested at the 52-week low of $92.99.

- A weekly close below it breaks a 17-year structure and removes the setup entirely.

Targets if it confirms

- First: $143, the 52-week high.

- Second: $165, the 2025 swing high.

- The full pattern measured move exceeds $300 — arithmetically valid, but not a usable target.

Timeframe and summary

- A pattern eight years in the making can take quarters to resolve, not weeks.

- Q2 results are due 30 July — the most likely catalyst for which side gives way.

- Above $120 it's a breakout. Below $93 it's broken. In between, it's still consolidating.

Confidence: high on the levels, low on timing.

G

Trade Idea - Clorox Below $100—Bear Flag Points to $69 Target

CLX has been declining since early 2022, and the weekly chart shows more downside likely. Trading under $100 for the first time in years, price is forming a bear flag—a consolidation pattern that typically breaks lower.

The setup traces to a head-and-shoulders pattern (2018–2022) that triggered when price broke the neckline in January 2022. That measured move targets $69.34, down from $160+.

The flag's lower boundary sits near $84.70. A daily close below that confirms the breakdown and raises odds of hitting the $69 target. Until then, it's just consolidating within the larger downtrend.

If $69 holds, watch overhead resistance at $101.82 (declining trendline) and $132.59 (longer-term trendline)—both former selling zones.

This is a slow-moving setup: years to form, years to play out. Below $84.70, the bear flag confirms. Above it, consolidation continues. The $69 target remains open.

J

QQQ Market Structure Is Shifting—What Comes Next?

- QQQ is showing early signs of a potential trend reversal, with price losing momentum after making new highs. The recent lower highs and increasing selling pressure suggest the market is attempting to shift from a bullish trend toward a more bearish structure.

- The chart has broken down from a key technical pattern, signaling that buyers are losing control. Unless price quickly reclaims the broken structure, the probability of further downside remains elevated.

- The $690–685 support zone is the most critical level to watch. A decisive daily close below $685 would confirm the bearish breakdown and could accelerate selling pressure.

- If $685 fails, QQQ may extend its downside move toward the next major support near $650, as the breakdown would invalidate the recent consolidation and strengthen the bearish trend.

- However, if buyers step in and QQQ reverses sharply by the end of the session, closing back above today's open with strong momentum, today's selloff could be interpreted as a bear trap, trapping short sellers and signaling renewed bullish strength.

- A strong bullish reclaim from current support could shift market sentiment back in favor of the bulls, increasing the probability of another rally toward the all-time highs. Until either $685 breaks or resistance is reclaimed, expect elevated volatility and confirmation before committing to a directional bias.

J

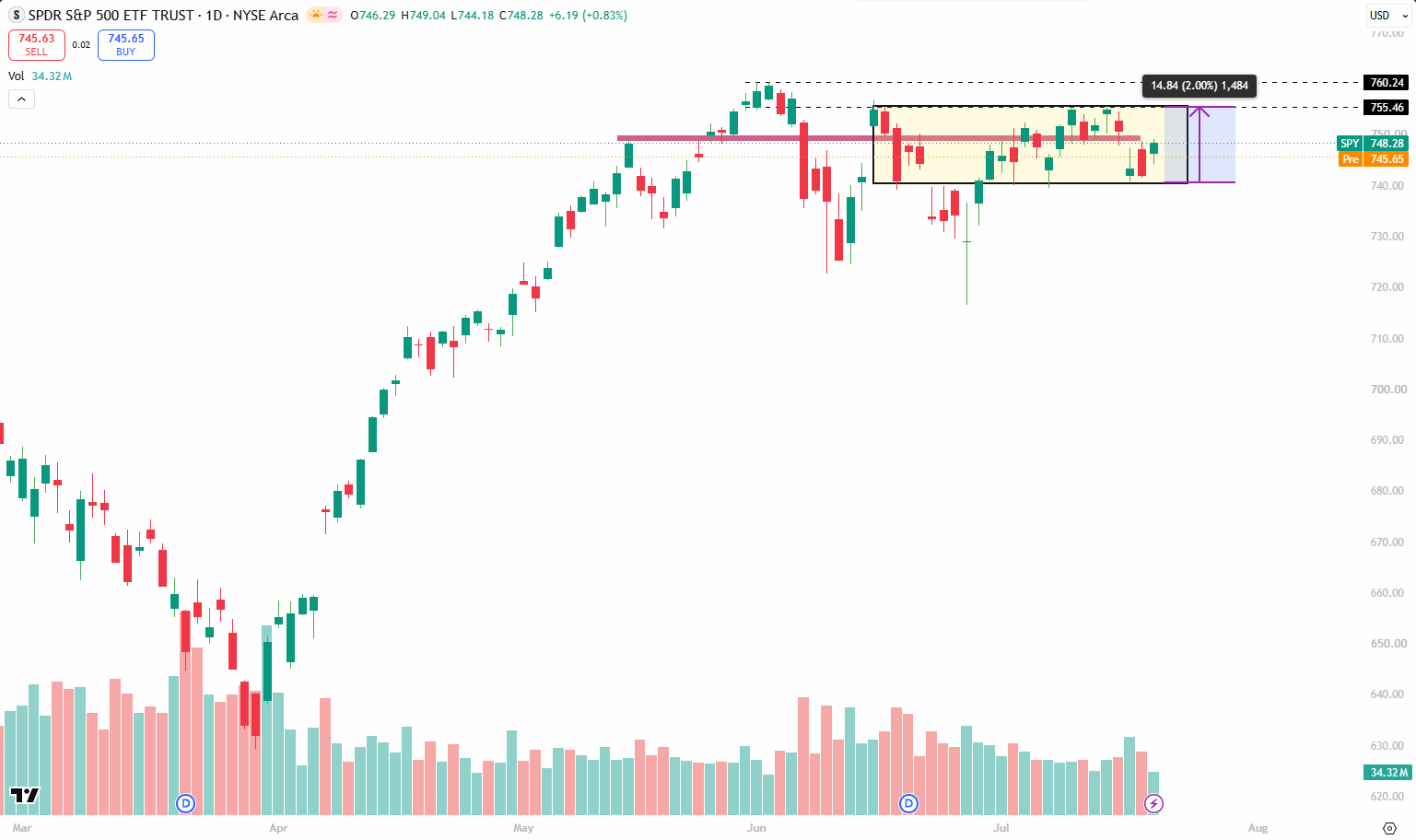

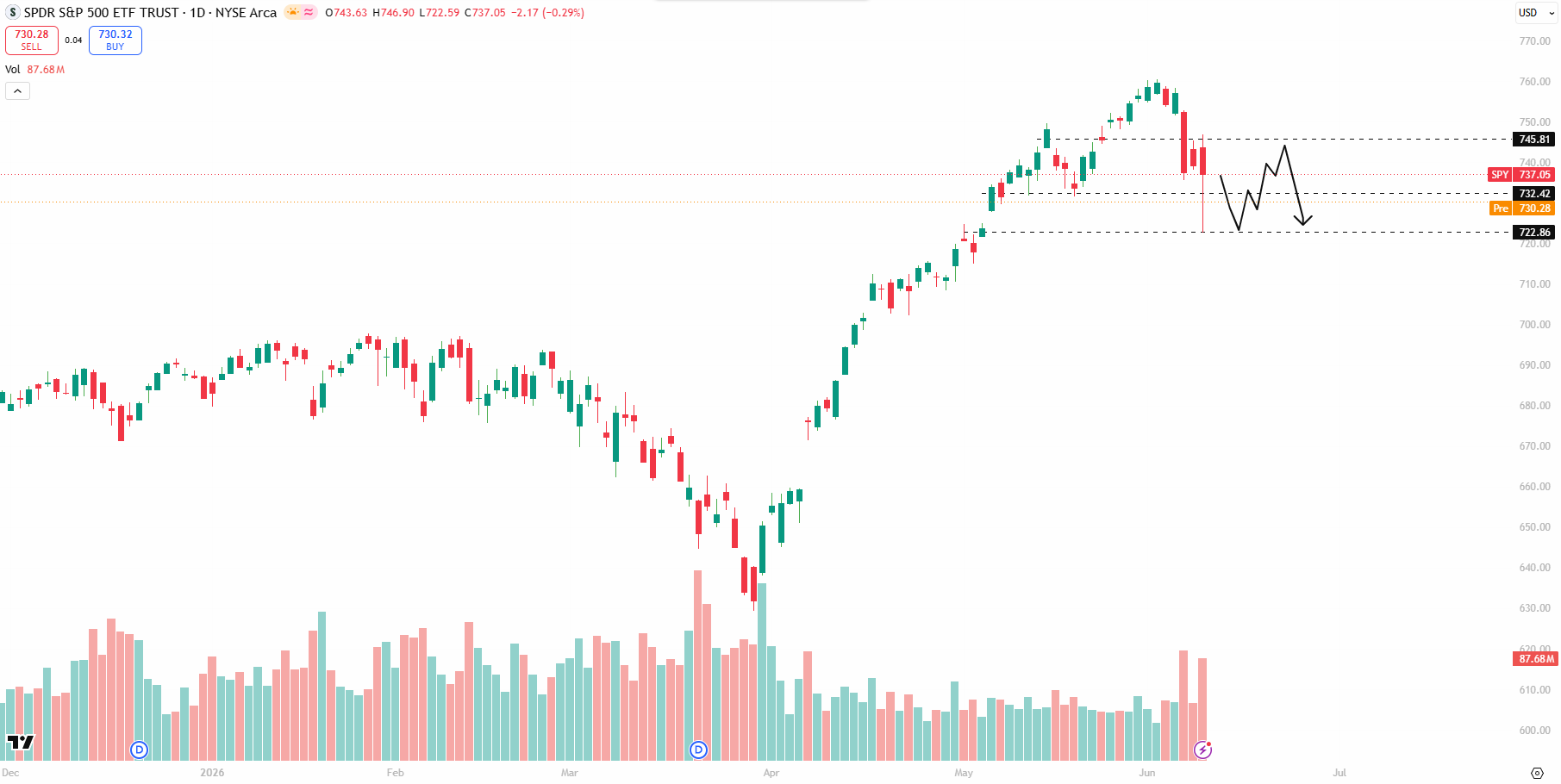

S&P 500 - SPY Stuck in a 2% Range: Breakout or Breakdown Ahead?

- SPY remains in a consolidation phase, trading within a 2% range between 740 and 755, with neither buyers nor sellers taking decisive control.

- The broader trend remains bullish to sideways, as price continues to hold above key support despite recent geopolitical and macro uncertainty.

- There is no confirmed bearish trend at this stage. A sustained close below 740 would be needed to signal a meaningful shift in market structure.

- Expect elevated volatility as investors react to earnings, geopolitical developments, and tariff-related headlines over the coming sessions.

- Be cautious of fake breakouts and breakdowns. Until SPY delivers a decisive move above 755 or below 740, range-bound price action is likely to trap both bulls and bears.

J

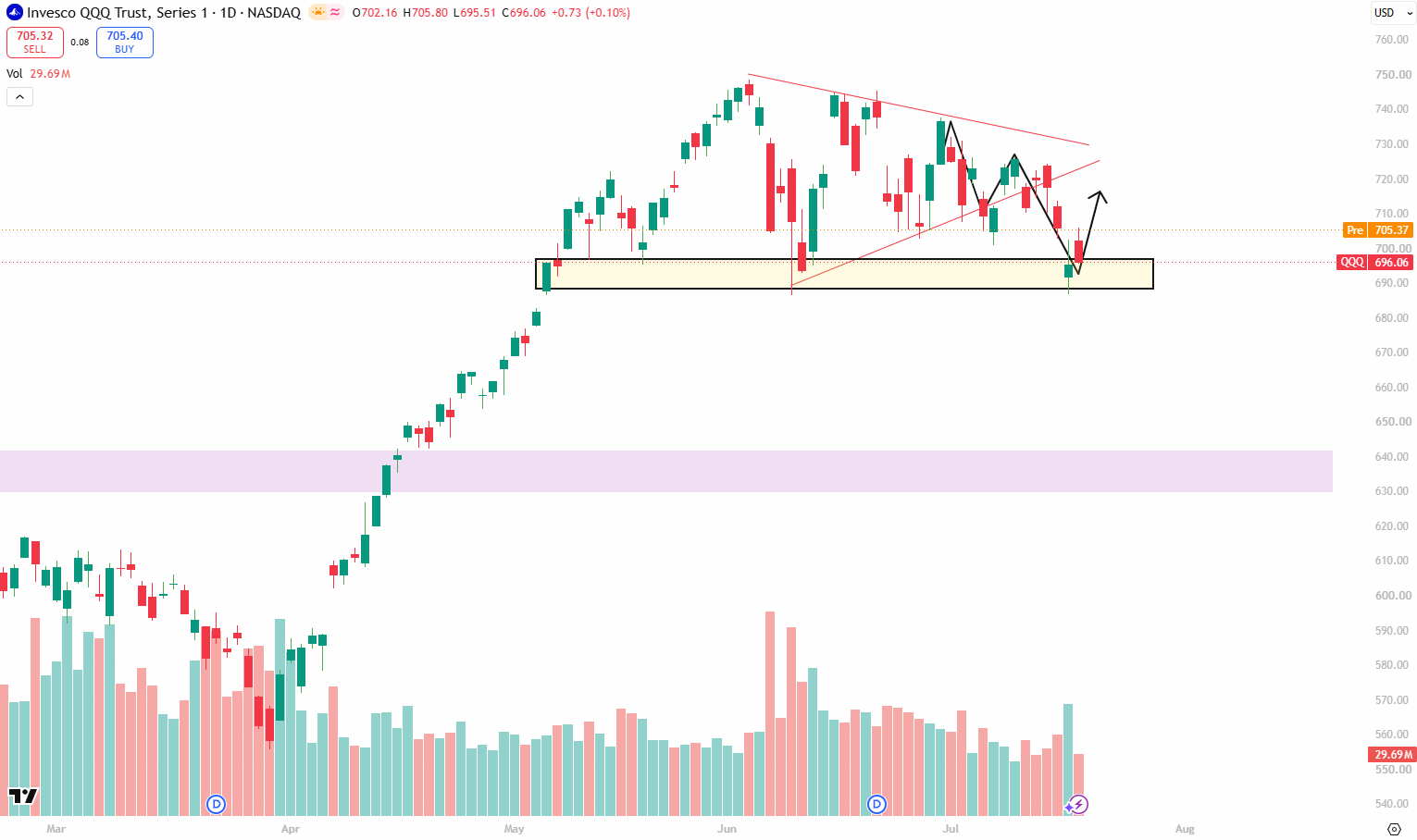

QQQ Daily Chart Analysis - 21 July

- Major demand zone: 690–695 remains the key support area (highlighted box). Buyers have defended this level multiple times, making it the most important zone to watch.

- Triangle structure still in play: Price is trading within a descending triangle / contracting range, with falling resistance around 725–730 and rising support that has now been tested near the demand zone.

- Expected short-term bounce: As long as 690 holds on a daily closing basis, QQQ could stage a relief rally toward 705, followed by 715–720, with 725–730 acting as the major resistance zone.

- Resistance levels: Initial resistance lies at 705–710. A successful move above this area opens the door to 720–725, while a breakout above 730 would invalidate the current bearish structure.

- Bearish risk: A daily close below 690 would confirm a breakdown from the demand zone and increase the probability of further downside toward 675–680, with the next major support near 630–635.

- Trading bias: The current setup favors a buy-the-dip bounce from support, but confirmation is needed through higher highs and stronger volume. Until 730 is reclaimed, the broader trend remains neutral to slightly bearish within the consolidation pattern.

J

Trump Announces 50% Tariffs on Canadian Imports

Trump Announces 50% Tariffs on Canadian Imports

* President Trump unveiled 50% tariffs on a broad range of Canadian imports, including beer, dairy products, chemicals, and hockey equipment, accusing Canada of unfair trade practices.

* Canadian oil remains exempt from the tariffs, which are scheduled to take effect in 30 days. Markets remain cautious as analysts warn the move could trigger retaliatory measures and further escalate trade tensions.

J

S&P 500 (SPY) ETF's 4H Technical Analysis: Bullish Structure Still Intact

- Ascending Channel Remains Intact: Price continues to respect the rising channel, keeping the short-term trend bullish as long as it holds above the lower trendline support.

- Key Demand Zone Holding: The highlighted 748–749 support zone has repeatedly attracted buyers. A successful retest of this area could provide the foundation for the next leg higher.

- Healthy Pullback Before Continuation: The projected path suggests a brief pullback into support before buyers regain control. This would be a typical bullish retest rather than a trend reversal.

- Resistance to Watch: SPY is trading just below the 755–760 resistance area. A decisive breakout above this range would confirm renewed momentum and increase the probability of a move toward the upper boundary of the channel.

- Upside Target Near Channel Resistance: If the bullish scenario plays out, price could rally toward the 766–768 region, where the upper trendline is likely to act as the next major resistance.

- Bullish Bias Above Support: The overall structure remains constructive while price stays above 748. A breakdown below this demand zone and the lower channel trendline would invalidate the current bullish outlook and shift momentum in favor of sellers.

J

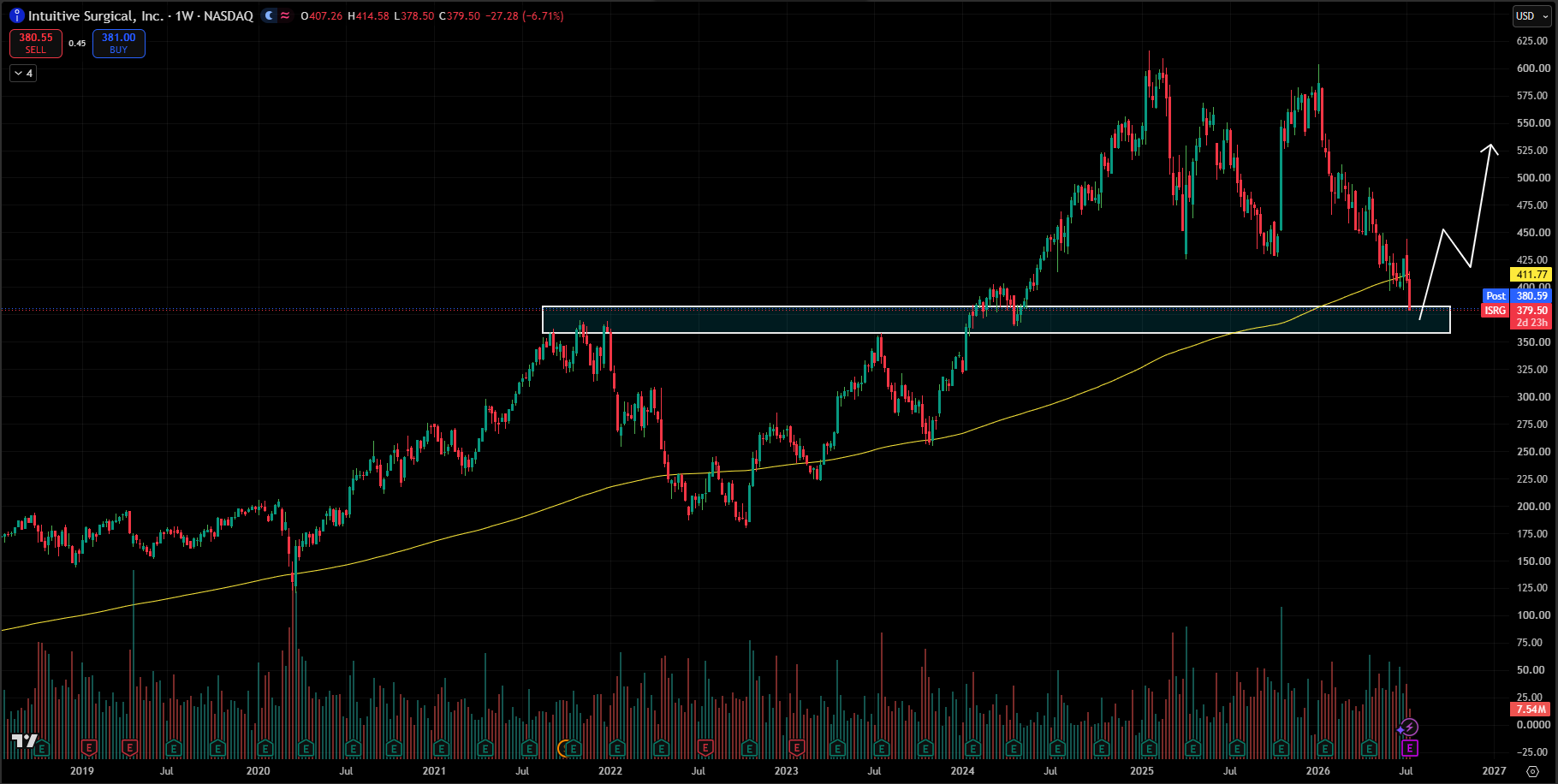

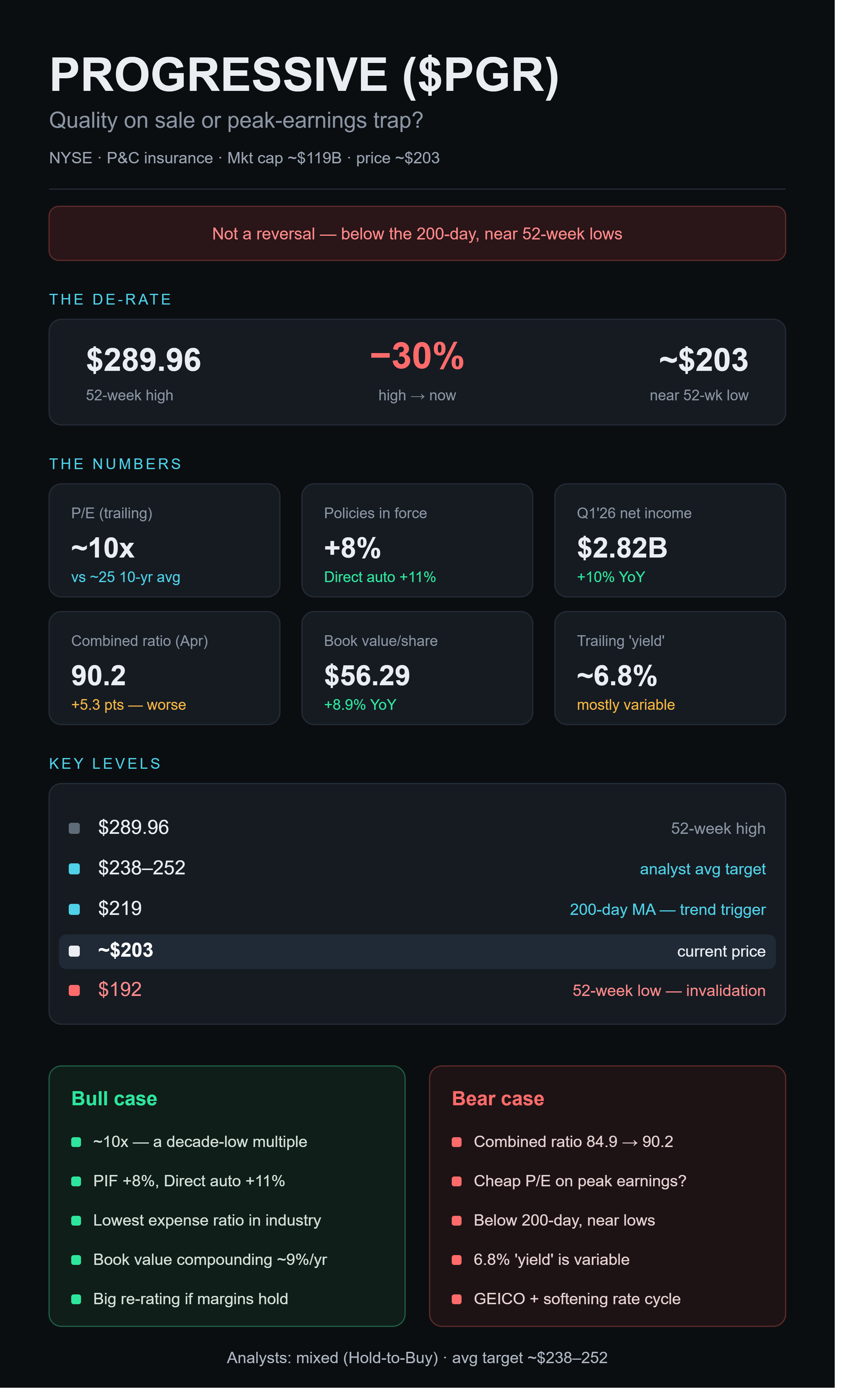

ISRG Long: 20% Grower, Net Cash, ~45x - Widest Multiple Discount in 5 Years

Intuitive Surgical (ISRG, NASDAQ) — Buy-Side Equity Long Note

Data current as of July 14, 2026 close. Last reported quarter: Q1 2026 (April 21, 2026). Q2 2026 results are due July 16, 2026 — not yet available at writing.

- BUY / accumulate. ISRG is a dominant, wide-moat robotic-surgery franchise growing revenue ~20%+ with 86% recurring revenue, ~$8B net cash and no debt, now trading ~$407 — down ~28% YTD and near a 52-week low ($396.68). The multiple has compressed to ~49x trailing / ~45x forward P/E, well below its 5-year averages (~69–73x trailing, ~57x forward), creating an attractive entry into a structurally superior compounder.

- The selloff is sentiment-driven, not fundamentals-driven. Q1 2026 revenue rose 23% to $2.77B, procedures grew 17%, installed base grew 12% to 11,395 systems, and management raised procedure guidance. The drawdown reflects tariff/margin fears, a Class I stapler recall, GLP-1 bariatric worries, China competition, and sector-wide multiple compression — most of which are manageable or overstated.

- Catalysts ahead: Q2 2026 earnings July 16; da Vinci 5 upgrade cycle + cardiac clearance; potential IEEPA tariff refunds. Consensus target ~$561–585 (~38–44% upside), range $366 (Deutsche Bank, Sell) to $750 (Bernstein). Key risks: durable procedure deceleration below ~13% and margin erosion.

Key Findings

- Price/valuation: ~$407 (July 14, 2026), market cap ~$144B, EV ~$140B. Trailing P/E ~49x, forward P/E ~45x, P/B ~8.2x, EV/EBITDA ~35x. All below 5-year averages.

- Business: da Vinci surgical systems + Ion endoluminal (lung biopsy) + digital ecosystem. Razor/razor-blade model — 86% recurring revenue.

- Growth: FY2025 revenue $10.06B (+20.5%); net income $2.86B (+23%); da Vinci procedures +18%. Q1 2026 accelerated to +23% revenue.

- Balance sheet: ~$8.0B cash & investments, zero long-term debt, ~$1.7B remaining buyback authorization, no dividend.

- Bearish narratives: tariffs (~1.0% of 2026 revenue), China competition, GLP-1 bariatric decline (<3% of US da Vinci procedures), Class I SureForm stapler recall, new competition (Medtronic Hugo, J&J Ottava).

Details

1. Current Price & Valuation

As of the July 14, 2026 close, ISRG traded at $407.12 (previous close $406.78), near its 52-week low of $396.68 and far below the 52-week high of $603.88. Market cap ~$144.2B; enterprise value ~$139.6–140B. The stock is down roughly 27–28% year-to-date and off ~30% from its January 2026 peak above $600. Average daily volume ~2.3–2.5M shares; beta ~1.46–1.68.

Valuation multiples (current vs. 5-year history):

- Trailing P/E: ~49x (TTM EPS ~$8.22). 5-year average ~69–73x (clustered tightly across FinanceCharts 72.9x, Public 72.2x, FullRatio 69.3x); 10-year average ~61x. Current multiple is near the low end of its historical range — a meaningful de-rating.

- Forward P/E: ~45x vs. 5-year average forward P/E ~57x (Intellectia).

- P/B: ~8.2x (GuruFocus, July 14) to ~9.6x (StockAnalysis) vs. 5-year average ~9.6x — now near/slightly below average.

- EV/EBITDA: ~35x implied currently vs. FY2021–25 average ~56x (range ~43x–71x).

- P/FCF: ~54x (GuruFocus) or ~114x (FinanceCharts) — wide source discrepancy from differing FCF definitions; 5-year average ~137x (FinanceCharts) / 10-yr median ~67x (GuruFocus). Both frameworks show current below average.

- PEG: ~2.1–2.7x.

Peer comparison (mid-2026 forward P/E): ISRG ~45x carries a large premium to Medtronic (MDT) ~13x, Boston Scientific (BSX) ~13x forward (trailing ~20x), Stryker (SYK) ~21x forward (trailing ~35x), and Edwards Lifesciences (EW, trailing ~42x). On EV/EBITDA, EW ~22x and MDT ~14–15x sit well below ISRG. The premium reflects ISRG's ~20%+ revenue growth (vs. MDT ~10%, SYK ~3%, EW ~9–11% in the most recent comparable quarter), 86% recurring revenue, and a net-cash balance sheet. Critically, that premium has narrowed sharply in 2026 as ISRG de-rated while the business kept compounding — the core of the long thesis.

2. Business Fundamentals

Intuitive Surgical is the pioneer and dominant player in robotic-assisted surgery. Products:

- da Vinci surgical systems (multiport Xi/X, next-generation da Vinci 5, and single-port SP) for urologic, gynecologic, general, cardiothoracic, and head/neck surgery.

- Ion endoluminal system — robotic bronchoscopy for minimally invasive lung biopsy.

- Digital ecosystem — My Intuitive, SimNow, Case Insights, telepresence/telecollaboration.

Revenue mix (razor/razor-blade): In Q1 2026, instruments & accessories were $1.686B (61% of revenue), systems $651M (23%), services $434M (16%). Recurring revenue (I&A + services) is ~86% of total — the crux of the thesis, since it scales with procedure volume rather than one-time capital sales and produces high revenue visibility.

Most recent results (Q1 2026, reported April 21, 2026):

- Revenue $2.77B, +23% YoY (vs. $2.25B; beat ~$2.62B consensus). I&A +23%; systems +24% to $651M.

- GAAP net income $822M / $2.28 diluted EPS; non-GAAP net income $901M / $2.50 EPS (vs. $1.81 prior year, +38%; beat ~$1.92–2.11 estimates).

- Worldwide procedures +17%; da Vinci +16% (to ~847,000 cases), Ion +39% (to ~42,700 cases).

- Placed 431 da Vinci systems (232 were da Vinci 5) vs. 367 prior year; 52 Ion systems.

- Installed base 11,395 da Vinci (+12% from 10,189) and 1,041 Ion (+22%).

- Non-GAAP gross margin 67.8%; non-GAAP operating income $1.08B (~39% margin).

- Instrument/accessory revenue per procedure rose to ~$1,880 from ~$1,780 as da Vinci 5 mix increased.

Full-year 2025: Revenue $10.06B (+20.5%); net income $2.86B (+23%); da Vinci procedures +18%; 1,721 da Vinci systems placed (870 da Vinci 5); ~3,153,000 da Vinci procedures. Non-GAAP gross margin ~67.6%; operating margin ~29% GAAP / ~37–39% non-GAAP; net margin ~28%.

5-year revenue trend: 2021 $5.71B → 2022 $6.22B → 2023 $7.12B → 2024 $8.35B → 2025 $10.06B. Net income: 2022 $1.32B → 2023 $1.80B → 2024 $2.32B → 2025 $2.86B. Consistent ~20% top-line and 20%+ EPS growth.

da Vinci 5 rollout: Launched 2024. Per Intuitive's May 21, 2026 release, more than 1,400 da Vinci 5 systems have been installed globally, with more than 380,000 procedures performed by more than 12,800 surgeons in 10 countries. da Vinci 5 has ~10,000x the computing power of the Xi; it carries utilization roughly 11% higher than the Xi (per TIKR), a key economic driver since higher utilization compounds recurring revenue. 100+ software/hardware updates began rolling out in June 2026 (telepresence, mobile login, SimNow 2, digital ruler); extended-use Force Feedback instruments (6→15 uses) improve procedure economics. FDA cleared da Vinci 5 for certain cardiac procedures (mitral valve repair, IMA mobilization) in early 2026 — a new addressable market (~160,000 US/S. Korea procedures cited).

Ion: >325,000 procedures since launch; installed base 1,041 (+22%); procedure growth ~39–51%.

Returns/cash: ROE ~16–17%, ROIC ~24.8%. FY2025 free cash flow ~$2.5B (+91% YoY); TTM FCF ~$2.3–2.8B. Strong earnings-to-cash conversion. R&D ~$1.3B (14.5% of sales, +14.5% YoY).

3. Balance Sheet & Capital Returns

- Cash & investments: ~$8.0B at Q1 2026 ($9.0B at YE2025); zero long-term debt. Interest coverage effectively not applicable (net cash generates positive interest/other income ~$85M/quarter). Total assets $20.11B, total liabilities $2.51B, stockholders' equity $17.6B (Q1 2026 10-Q). Excellent liquidity.

- Dividend: None — ISRG has never paid a dividend, reinvesting in growth. Payout ratio N/A.

- Buybacks: Board authorized $13.0B cumulative since 2009; raised the program to $5.0B in mid-2025 (~$1.7B remaining at YE2025). Repurchased 4.8M shares at avg $477.84 in 2025; 2.3M shares for $1.1B in Q1 2026. Shares outstanding ~355M, down slightly YoY. Capital return is entirely via buybacks.

4. Recent News, Catalysts & Sentiment

- Q2 2026 earnings: July 16, 2026 (after close). Consensus ~$2.82B revenue, ~$2.48–2.50 EPS (~15%/13% YoY growth).

- Selloff drivers: sector-wide multiple compression / capital rotation from medtech into AI; tariff and margin fears; the Class I SureForm stapler recall; GLP-1 bariatric concerns; China competition; and a late-May fear about OpenAI entering robotics (widely regarded as overdone, since it targets humanoid/general-purpose robots, not soft-tissue surgery).

- Recall: FDA Class I recall of 8mm SureForm 30 gray stapler reloads (incomplete staple lines on blood vessels). Per FDA's notice, as of February 23, 2026, Intuitive reported four serious injuries and one death associated with the issue; the death occurred in late December 2025 and Intuitive sent its removal letter March 11, 2026. Separately, multiple Class II recalls of reusable da Vinci instruments (cable fraying/breakage). The company says suitable alternatives are available (blue/white reloads still usable) and root cause is under investigation. Reputational/regulatory overhang, but limited direct financial impact given the affected SKU is a small slice of I&A.

- Analyst ratings: Consensus Buy (~23 Buy, 9 Hold, 2 Sell). S&P Global (34 analysts): average target $561.84; Benzinga (28 analysts): consensus $585.48, high $750 (Bernstein, Jan 23, 2026), low $366 (Deutsche Bank, Sell, cut from $440 in early June). Implied upside ~38–44%. Recent target cuts kept ratings intact: TD Cowen $585→$520 (Buy), Evercore $480→$430 (In-Line), BofA $650→$520 (Buy) — valuation resets, not thesis breaks. BMO initiated Outperform $518 (July 9); Goldman Sachs publicly defended the stock (July 3).

- Tariffs: 2026 guidance embeds a ~1.0% of revenue tariff hit (down from 1.2% at Q4). Exposure: US-China (~50%), German endoscopes (~40%), Mexico (~10%). Q1 2026 tariff cost was ~$28M in COGS. The February 2026 US Supreme Court ruling that IEEPA tariffs are unconstitutional, plus the CBP refund portal launched April 2026, create refund/upside optionality.

- China: Small (only 4 da Vinci placements in Q1 vs. 226 US, 117 Europe) but structurally challenged — domestic competitors winning tenders, 125% tariffs on imported Xi systems, and no robotic reimbursement clarity expected until 2027. Total OUS procedures still grew ~20%.

- GLP-1: US bariatric volumes down high-single-digits for six consecutive quarters; now <3% of US da Vinci procedures. Management frames GLP-1s as a near-term headwind rather than displacement (adherence/cost/side-effect issues limit long-term drug retention) and says it continues gaining bariatric share. MDT and Teleflex face the same dynamic.

- Competition: Medtronic Hugo received FDA clearance December 3, 2025 "for use in minimally invasive urologic surgical procedures including prostatectomy, nephrectomy, and cystectomy — common procedures that account for about 230,000 surgeries per year in the U.S." (pursuing general surgery/gynecology next). J&J Ottava submitted for FDA de novo (general surgery) January 2026. CMR Surgical (Versius) and others are also entering. ISRG's moat: >11,000 installed systems, ~17M cumulative procedures, a two-decade clinical/regulatory lead, deep switching costs, and an entrenched training ecosystem.

- 2026 guidance (raised at Q1): da Vinci procedure growth 13.5%–15.5% (up from 13–15%); non-GAAP gross margin 67.5%–68.5% (incl. ~1.0% tariff impact); non-GAAP opex growth 11–14%. Q1's 17% procedure growth ran above the full-year guide, suggesting conservatism.

5. Technical Data

- Trend: Downtrend / near 52-week lows. At ~$407 the stock sits below both its 50-day (~$414) and 200-day (~$424–494 depending on source/method) moving averages — a bearish posture. Most technical services flag "Sell/Strong Sell."

- 52-week range: $396.68 – $603.88.

- Support: ~$396–400 (52-week low / round number). Resistance: ~$414 (50-day), then ~$424–430 (200-day), then ~$450.

- Momentum: RSI has ranged oversold-to-neutral (~33–60) across recent dates, with stabilization/bounce attempts near lows. Distribution signs: insiders were net sellers over the past six months (38 sales, 0 buys — routine but adds caution), and large institutions (e.g., Northwestern Mutual, BlackRock, Amundi) trimmed positions. No clear accumulation signal yet; a reclaim of the 50-/200-day averages would mark a trend improvement.

6. Filings

- 10-K (FY2025): filed February 3, 2026. Confirms $13.0B cumulative buyback authorization; program raised to $5.0B mid-2025; ~$1.7B remaining at YE2025; 4.8M shares repurchased in 2025 at avg $477.84.

- 10-Q (Q1 2026, quarter ended March 31, 2026): total assets $20.11B, cash & investments $7.98B, inventory $1.95B, PP&E $5.45B, goodwill $613M, total liabilities $2.51B, equity $17.6B. Q1 tariff cost ~$28M in COGS. Details the IEEPA Supreme Court ruling and CBP refund portal, and flags China rare-earth/magnet export restrictions as a supply risk.

- 8-Ks: Q1 2026 earnings release (April 21); promotion of Taylor Patton to Chief Commercial & Marketing Officer (effective July 1); da Vinci 5 innovation announcements (May 21); da Vinci 5 cardiac clearance.

Recommendations

Stage 1 — Initiate/accumulate now (starter position). At ~$407, ~45x forward earnings for a ~20% grower with 86% recurring revenue, net cash, and a widening moat is attractive relative to ISRG's own history (~57x forward average). The drawdown is sentiment-led; fundamentals are intact (Q1 revenue +23%, guidance raised). Given negative technical momentum and near-term event risk, begin with a partial position rather than a full one.

Stage 2 — Add on confirmation at the July 16 Q2 print. Look for: (a) installed-base growth holding ≥12%; (b) procedure growth at/above the 13.5–15.5% guide; (c) non-GAAP gross margin defended within 67.5–68.5%; (d) no material recall/liability escalation. A clean print plus a reclaim of the 50-day (~$414) and 200-day (~$424) moving averages would justify completing the position.

Stage 3 — Full position on evidence that da Vinci 5 upgrade economics (higher utilization, Force Feedback ASPs, cardiac) are lifting recurring revenue per system, tariff refunds materialize, or China/bariatric headwinds stabilize.

Thresholds that would change the thesis (trim/exit):

- Procedure growth decelerating durably below ~13% (secular demand concern).

- Non-GAAP gross margin sustained below ~66% (structural margin erosion from tariffs/competition/pricing).

- Evidence that Hugo/Ottava are taking share at scale in core US urology/gynecology, or forcing instrument price wars.

- Escalation of the recall into a broad systemic quality/liability problem.

- Installed-base growth slowing below ~8–10%.

Price framework: Downside ~$366 (bear/Deutsche Bank) to ~$396–400 (technical support); base case consensus ~$560–585 (~38–44% upside); bull ~$675–750 on sustained 15%+ procedure growth and margin recovery.

Caveats

- Data recency: Price/technical data as of July 13–14, 2026; last reported quarter is Q1 2026 (April 21). Q2 2026 results (July 16) were not available at writing — the single most important near-term data point. Full-year 2025 and the 10-K are current (filed Feb 3, 2026).

- Valuation-multiple source conflicts: P/FCF varies ~2x across sources (54x vs. 114x) due to FCF definitions; P/B and EV/EBITDA "current" figures vary by measurement date as the stock fell from ~$504 (Feb) to ~$407 (July). Cited multiples are best-available approximations, not audited.

- Forward-looking items flagged: analyst price targets, "fair value" estimates, TIKR/Goldman scenarios, and 2026 guidance are projections, not facts. The most bullish scenarios (e.g., $500B market cap by 2031; $675–750 targets) are speculative and should be discounted accordingly.

- Technical "Sell" signals reflect momentum, not fundamentals; useful for timing, not for the thesis.

- Peer multiples (MDT, SYK, BSX, EW) are drawn from differing dates (May–July 2026) and definitions; treat as directional.

- GAAP vs. non-GAAP: ISRG's non-GAAP excludes large stock-based comp (~$210M/quarter); GAAP EPS is materially lower (Q1: $2.28 GAAP vs. $2.50 non-GAAP). Both are cited where possible; value the business on GAAP-inclusive economics before paying the non-GAAP multiple.

J

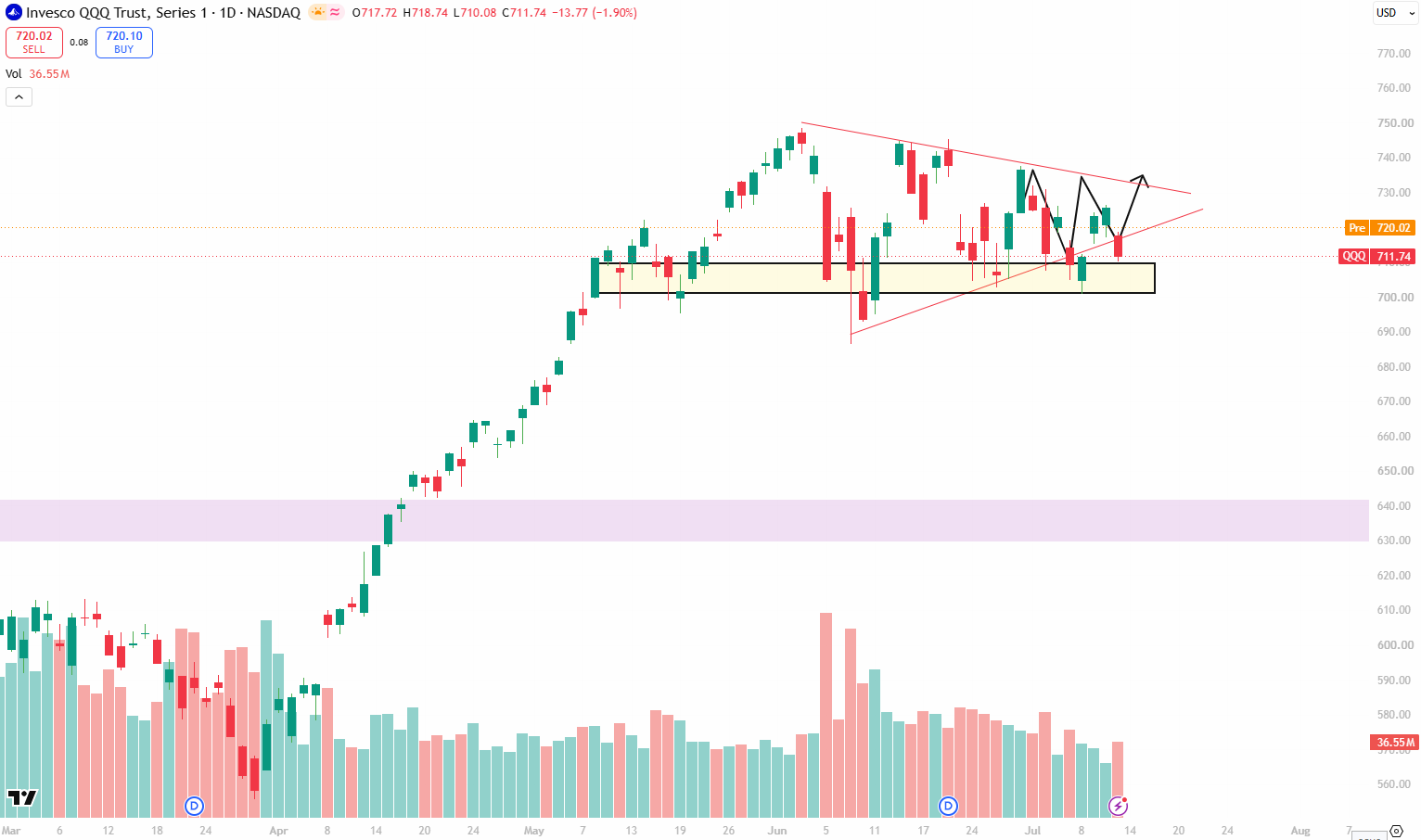

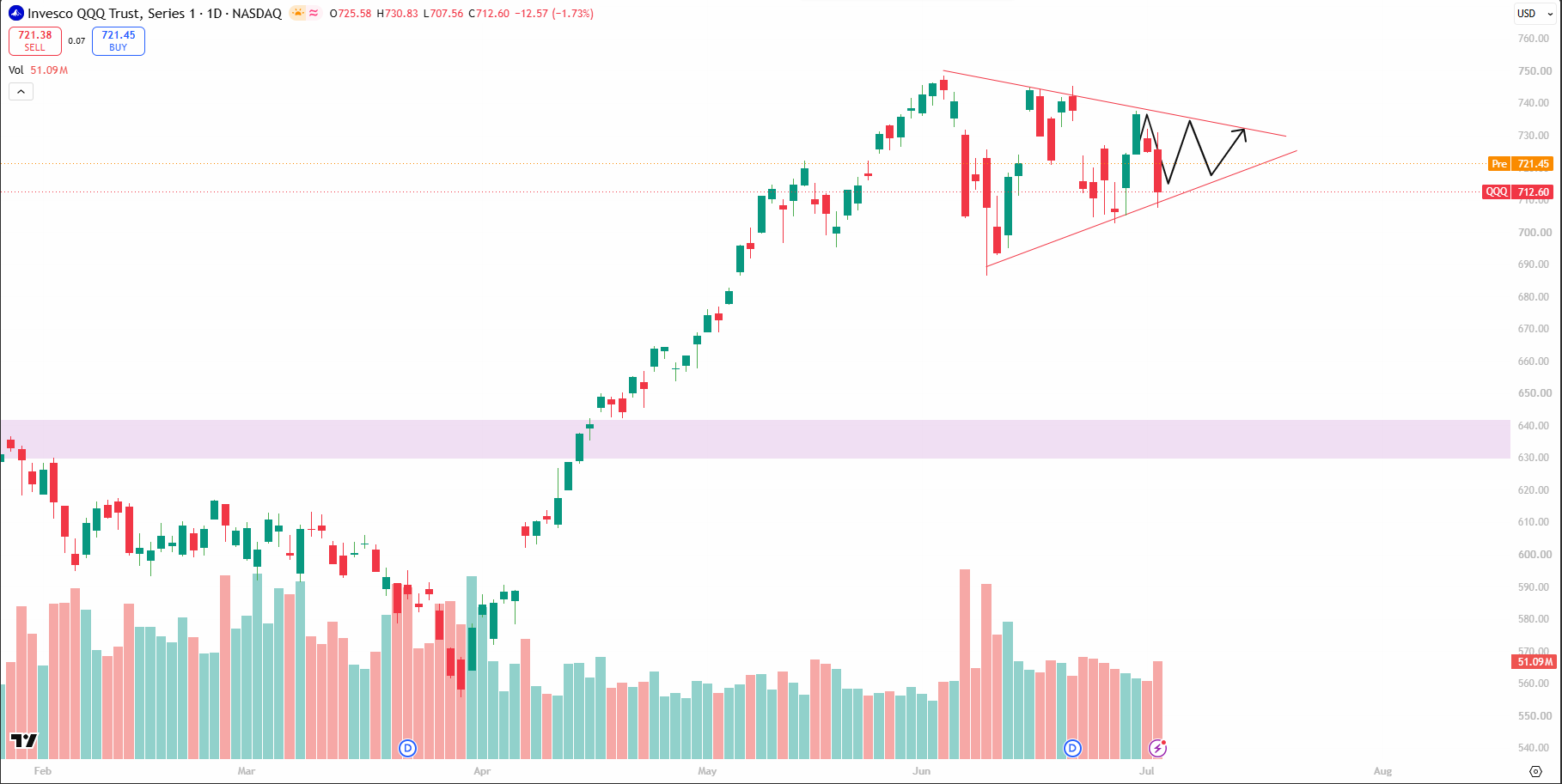

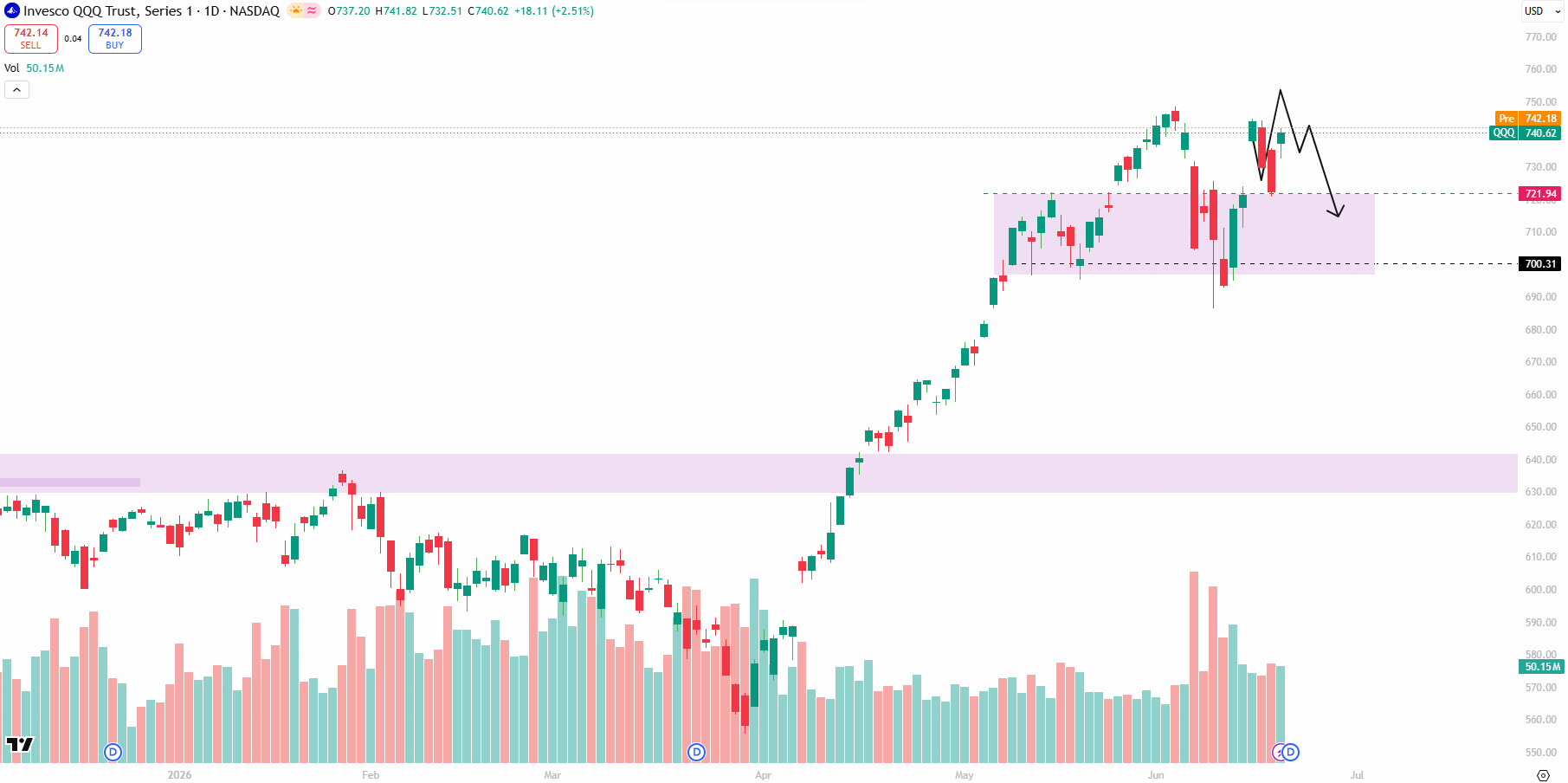

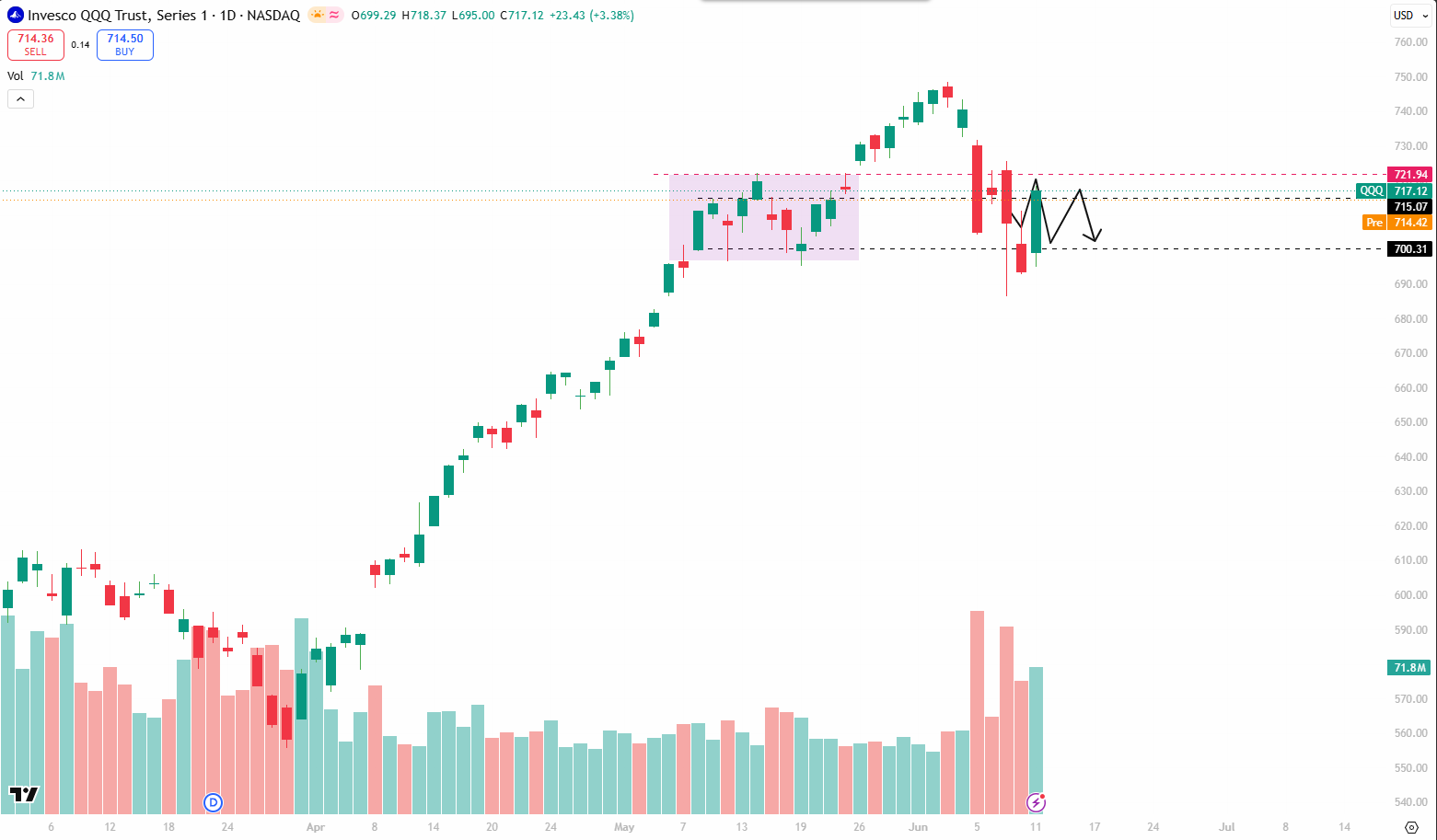

Bulls Defended the Line - NASDAQ (QQQ) Daily Technical Update

- Coiling triangle: price compressing between descending rail off ~750 and rising trendline off ~690. Apex ~725–730 this week — resolution imminent.

- Close was a test: -1.90% into 711.74 tapped the yellow box (~700–712) but held above the rising trendline. Wick-test, not a break.

- Pre-market reclaim: 720.02 (+1.2%) recovers the full support box. Looks like a shakeout / liquidity grab, not a breakdown.

- Drawn path = bullish continuation: buyers defend 705–710, then ABC advance toward the 730–735 upper rail.

- Upside trigger: daily close above 735 breaks the coil → re-opens 750, then measured-move targets.

- Invalidation: daily close below 700 kills it → exposes 690, then 630–642 (purple zone). Hard stop.

- Bias: cautiously bullish while 700 holds. Wait for a closing break — 735 long, 700 short. Don't front-run the wick.

J

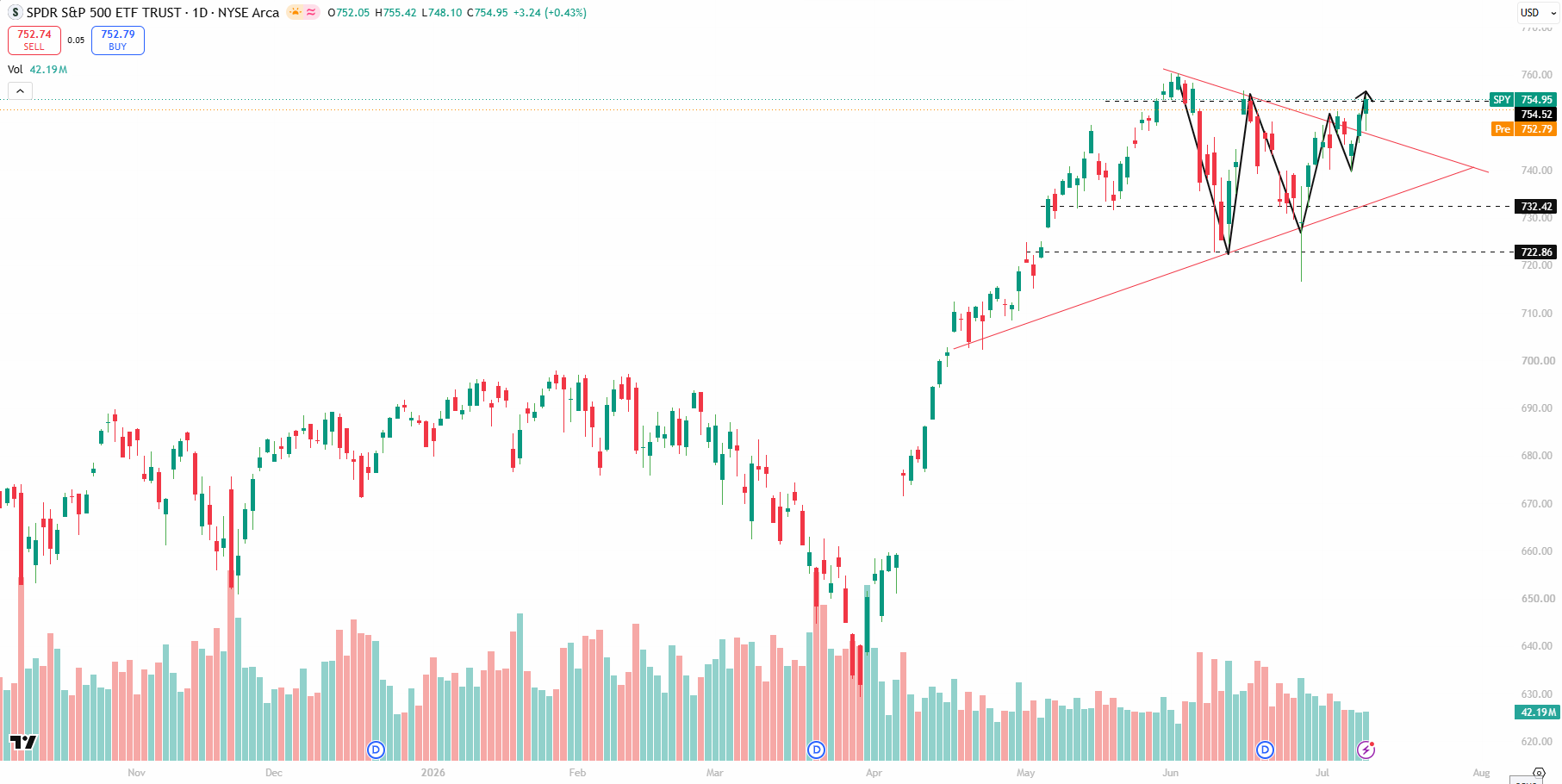

SPY Remains Constructively Bullish, Bull Flag Compression Points Toward New Highs!

Key Levels

- Resistance: $755-$757 → $763-$766 (All-Time High Zone)

- Immediate Support: $748-$750

- Major Support: $732

- Bias: Short-Term Bullish

- SPY continues to hold above the major support zone between $748-$755, with buyers consistently defending every pullback. The series of higher lows confirms that the primary uptrend remains intact despite recent volatility.

- Price is currently compressing inside a bullish continuation triangle (bull flag/pennant) after reclaiming the previous breakdown. This type of consolidation typically represents a pause before the next directional move rather than a trend reversal.

- The recent V-shaped recovery from the $722 support area demonstrates strong institutional demand, as sellers failed to sustain prices below the rising trendline. Each corrective move has been met with aggressive buying pressure.

- A decisive breakout and daily close above the $755-$757 resistance region would confirm the pattern and likely trigger a fresh momentum leg toward the previous all-time high, with an upside objective in the $763-$766 range.

- As long as SPY continues trading above the $748 support and the rising trendline remains valid, the short-term bias stays bullish. Only a sustained breakdown below $745, followed by a loss of $732, would weaken the current bullish structure and shift momentum in favor of the bears.

J

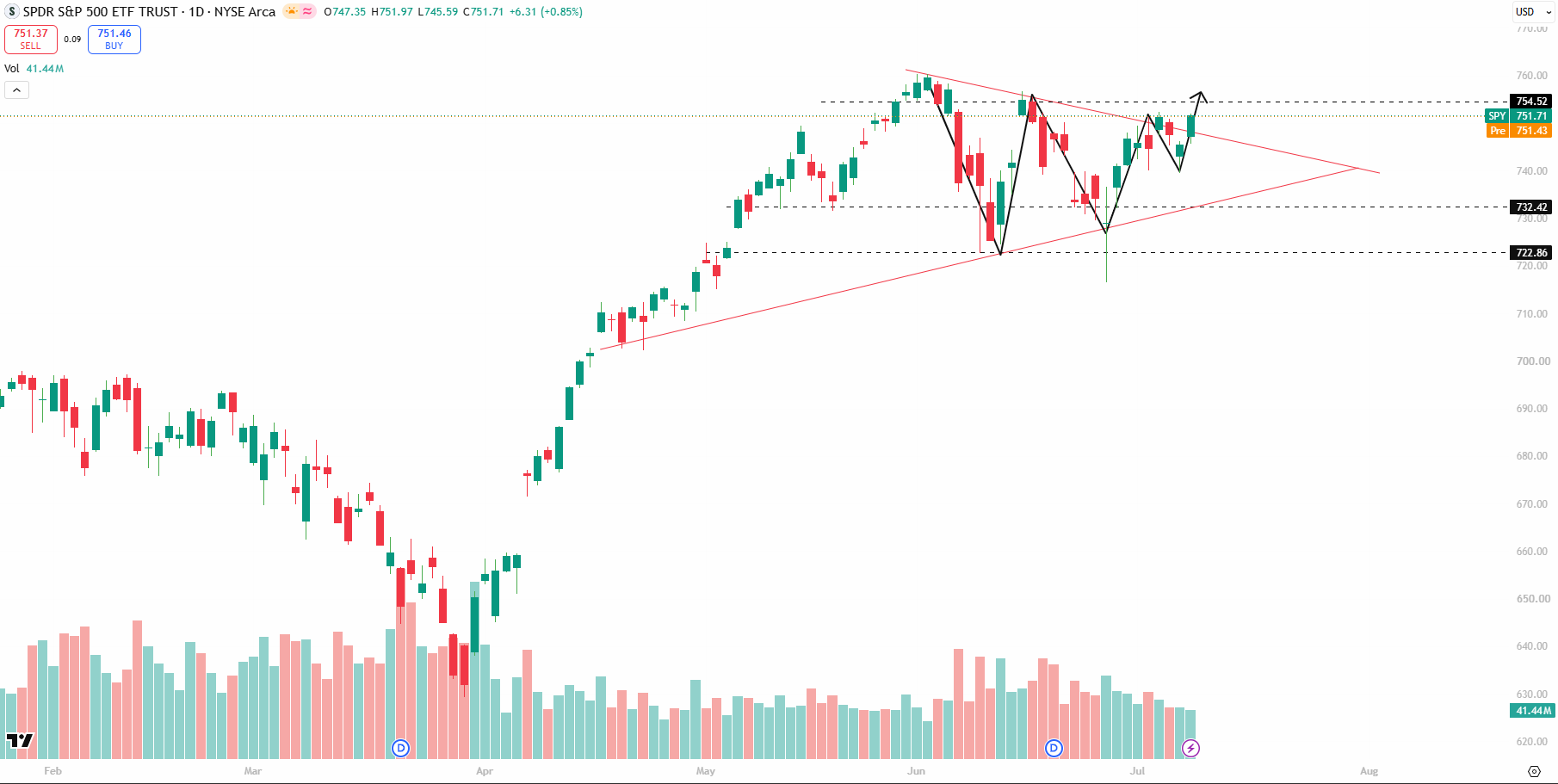

SPY Technical Update: Buyers Defend Key Zone, New High Incoming?

• SPY has followed our expected path, taking support from the lower trendline and showing a strong bounce back toward resistance levels.

• Price is currently trading near the $754 resistance zone; a breakout and daily close above this level may open the path for a new high.

• The formation continues inside a tightening range/triangle pattern, indicating consolidation before the next major move.

• As long as SPY holds above the $732–$722 support area, the overall structure remains bullish.

• A short-term range-bound movement is possible before buyers attempt the next upside breakout above the levels of $754.

A

J

NASDAQ (QQQ) Technical Analysis Update – Our Expected Move Playing Out

• QQQ has reacted exactly from our highlighted $700–$710 major support zone (yellow box), where we expected buyers to step in and defend this important demand area.

• The price successfully bounced from these levels, confirming that our previous analysis and support identification were accurate. Buyers continue to show strength around this zone.

• After the bounce, QQQ is now moving inside the expected short-term consolidation/range pattern, where price may continue sideways before deciding the next major directional move.

• As long as QQQ continues holding above the $700–$710 support region, the bullish structure remains intact and momentum could gradually shift back toward buyers.

• We may see some range-bound movement in the coming sessions, but a breakout above the current resistance trendline could open the path toward a new all-time high attempt.

• The immediate upside levels to watch remain around the $730–$750 resistance zone, where a breakout with strong momentum would confirm continuation of the bullish trend.

• A daily close below the $700 level would be the key invalidation point and could increase the chances of a deeper correction toward lower demand areas.

• Overall, QQQ is following our projected roadmap so far — support held, bounce confirmed, and now the market is entering the next phase where a breakout could trigger the next bullish leg higher.

J

SpaceX (SPCX): The Best Business I Wouldn't Buy - Love the Company, Fear the Price

SpaceX (SPCX): Great Company, Brutal Price

My breakdown of the biggest IPO in history, now that the dust has settled.

SpaceX went public June 12 — the largest IPO Wall Street has ever done. Priced at $135, popped 19% to close Day 1 at $160.95 (~$2.1T cap), and as of July 7 it's back to ~$149 after sliding ~7% on its first day inside the Nasdaq-100.

My honest read: this is the best operating business in the space economy wearing one of the most demanding price tags on the market. Both things are true, and that tension is the whole story. Not financial advice — I'll repeat that at the end.

Snapshot

- SPCX on Nasdaq, ~$149, market cap ~$1.98T

- Range since listing: $135–$225.64 (no real 52-week range yet — one month of history)

- Loss-making today. Trades at roughly 100x sales.

What you're actually buying — three businesses

Starlink (the engine). ~60% of revenue and the only part that reliably makes money (+$4.4B operating profit in 2025). ~9,600 satellites, 160+ countries, 10M+ subscribers, ~97% of global satellite internet. They build the sats and the rockets that launch them, so nobody can match their pace. This is a genuine moat.

Launch (the strategic core). 165 Falcon 9 flights in 2025 — more than the rest of the world combined. Reusable boosters make everyone else look ancient. But it runs near breakeven because ~$3B/yr of Starship R&D flows through it. It's what makes everything else possible, not where the profit shows up.

AI (the wildcard and the wound). SpaceX absorbed xAI — Grok, the Colossus data centers, X — in February. It did $3.2B in revenue in 2025 and lost $6.4B doing it. This one segment is what turned a profitable company red, and it's carrying the bull case despite being the least proven piece.

The numbers

| ($B) | 2023 | 2024 | 2025 | Q1'26 |

|---|---|---|---|---|

| Revenue | 10.4 | 14.0 | 18.67 | 4.69 |

| Net income/(loss) | (4.6) | +0.79 | (4.94) | loss |

| Capex | 4.4 | 11.2 | 20.7 | ~7.7 (AI alone) |

Profitable in 2024 → lost ~$5B in 2025 after swallowing AI. Capex 5x'd in two years, almost entirely AI compute. 2025 by segment: Starlink +$4.4B, Launch −$0.7B, AI −$6.4B. Starlink is carrying the entire company.

Valuation — the part nobody wants to hear

At ~$1.98T on ~$18.7B revenue, that's ~100x sales while losing money. To grow into even a generous tech multiple (10–15x), revenue has to 8–9x from here.

Where the serious independent work lands vs. the market:

- Damodaran (independent DCF): ~$1.3T, roughly $100/share. Called the AI TAM claim close to "fantasy."

- Morningstar: ~$780B fair value — half the current cap.

- Street targets: $62 low to $800 high. Even the two IPO lead banks disagree by ~$1T (Morgan Stanley ~$300, Goldman ~$205).

Is the price justified? My answer: not here. The base case only works if you fully credit the AI story — the weakest, cash-hungriest, least-proven part. Strip AI out, value Starlink + launch on real cash flows, and you land near Damodaran/Morningstar, not the tape. You're buying a 20-year narrative priced as if it's already delivered.

Competition

- Launch: basically nobody. Blue Origin blew up a booster on the pad in May; Rocket Lab is a credible but tiny #2. China is the real long-term threat.

- Satellite internet: Amazon's Leo (ex-Kuiper) is the only deep-pocketed rival, and it's years behind — a few hundred sats vs. 9,600.

- AI: here SpaceX is the underdog. Grok trails OpenAI, Anthropic, Google. The most expensive segment is the one where they're least dominant.

Catalysts (next 12–36 mo)

- Aug 6: first public earnings and the first lockup unlock (20% of insider shares) — same day. Mark it.

- Starship V3 hitting real cadence — gates next-gen Starlink and the "AI data centers in space" pitch (targeted ~2028).

- Starlink direct-to-cell scaling + EchoStar spectrum deal.

- Wild card: JPMorgan floated a SpaceX–Tesla merger as "strategically sound." Nothing formal, but it's Musk.

Risks (ranked)

- Valuation — 100x sales, no room for error; independents say fair value is 35–60% lower.

- The AI segment — big losses, trailing rivals, load-bearing for the bull case.

- Founder control — Musk holds ~82% of the votes. You're a passenger.

- Capital intensity — $20B+/yr, FCF-negative until ~2031 (Goldman).

- Thin float + index mechanics — ~3–5% floating, now in the Nasdaq-100. That's why it swings 7% on a Tuesday.

- Regulatory/political — FAA, FCC, and the Musk-politics beta.

Bull vs. bear

- Bull: once-in-a-generation platform, dominates launch and broadband, free call option on space + AI. If even the base Street models hit, today is cheap.

- Bear: paying $2T (100x sales) for a company losing ~$5B/yr, burning $20B+/yr, FCF-negative for years, leaning on an AI unit behind every major lab — run by a founder with 82% of the votes.

- Suits: long horizon (5–10+ yrs), high risk tolerance, can stomach a 40% drawdown. Doesn't suit: anyone who needs current fundamentals to justify the price or wants a say.

Bottom line

Best asset in the space economy, one of the most demanding valuations on the board. Starlink is real and printing; launch is untouchable; the AI bet is expensive and unproven — and it's doing the heavy lifting in a $2T story.

I'm constructive on the business, cautious on the stock. Not a buyer up here — I'd want it dragged toward the $100–110 zone before risk/reward flips. Watch Aug 6: earnings and lockup land together, and that's when we find out what SPCX is worth once the hype has to share the room with a cash flow statement.

Size small. Respect the volatility. Don't let "I love the company" do your position-sizing.

J

NASDAQ (QQQ) Technical Analysis – Key Levels to Watch

- QQQ is currently testing a major support zone around $700–$710 (yellow box) where buyers previously stepped in, making this an important decision area.

- After the recent pullback from highs, price is forming a short-term consolidation pattern, and holding this support could trigger a bounce toward the upper resistance/trendline area.

- As long as QQQ stays above the $710 support region, the bullish structure remains intact and price may continue sideways before attempting another upside move.

- A daily close below $710 would signal weakness and increase the probability of a deeper correction toward the $700–$690 demand zone.

- Breaking below $700 could shift market sentiment bearish, as it would confirm a loss of key support and create more downside pressure on the technical chart.

- Overall, QQQ is at an important make-or-break level — buyers need to defend this zone to maintain momentum, while sellers will look for a breakdown confirmation.

A

Wall Street is back after the long Fourth of July weekend, and this week could bring several important market-moving events. Here's what investors should keep an eye on:

🔹 U.S. Services PMI: The services sector is expected to remain in growth mode. Since it makes up more than two-thirds of the U.S. economy, this report can influence market sentiment.

🔹 Fed Meeting Minutes: Investors will look for clues on inflation, interest rates, and the Federal Reserve's future plans under Chair Kevin Warsh.

🔹 Fed Task Forces: Markets are waiting for the announcement of outside experts who will help review the Fed's policies and operations.

🔹 Levi Strauss Earnings: Investors will watch how the company is handling tariffs, supply chain changes, and consumer demand.

🔹 Delta Air Lines Earnings: Lower oil prices could improve airline profits. Investors will focus on Delta's outlook for the rest of 2026.

A busy week with key economic data, Fed updates, and corporate earnings could shape market direction.

J

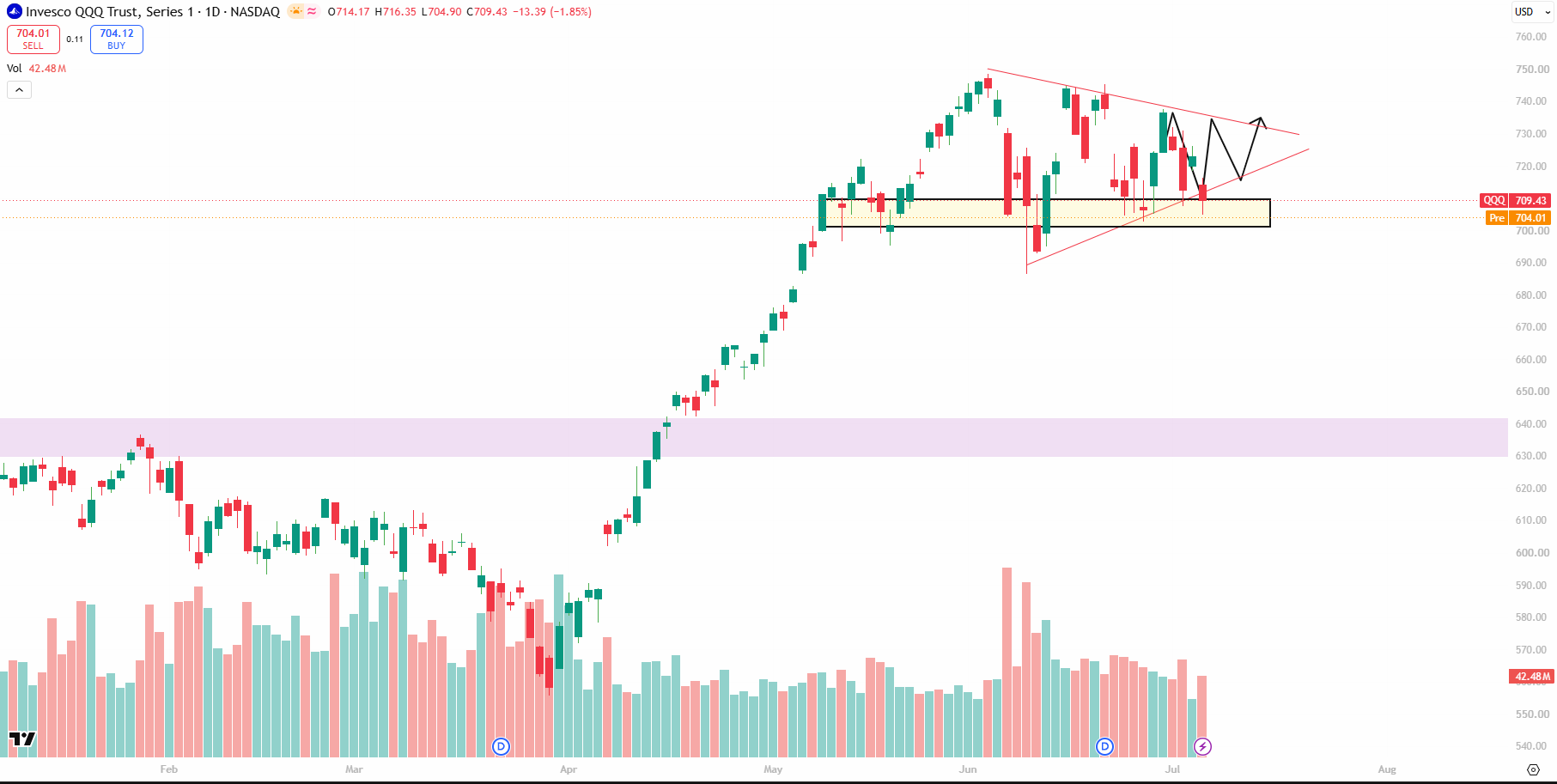

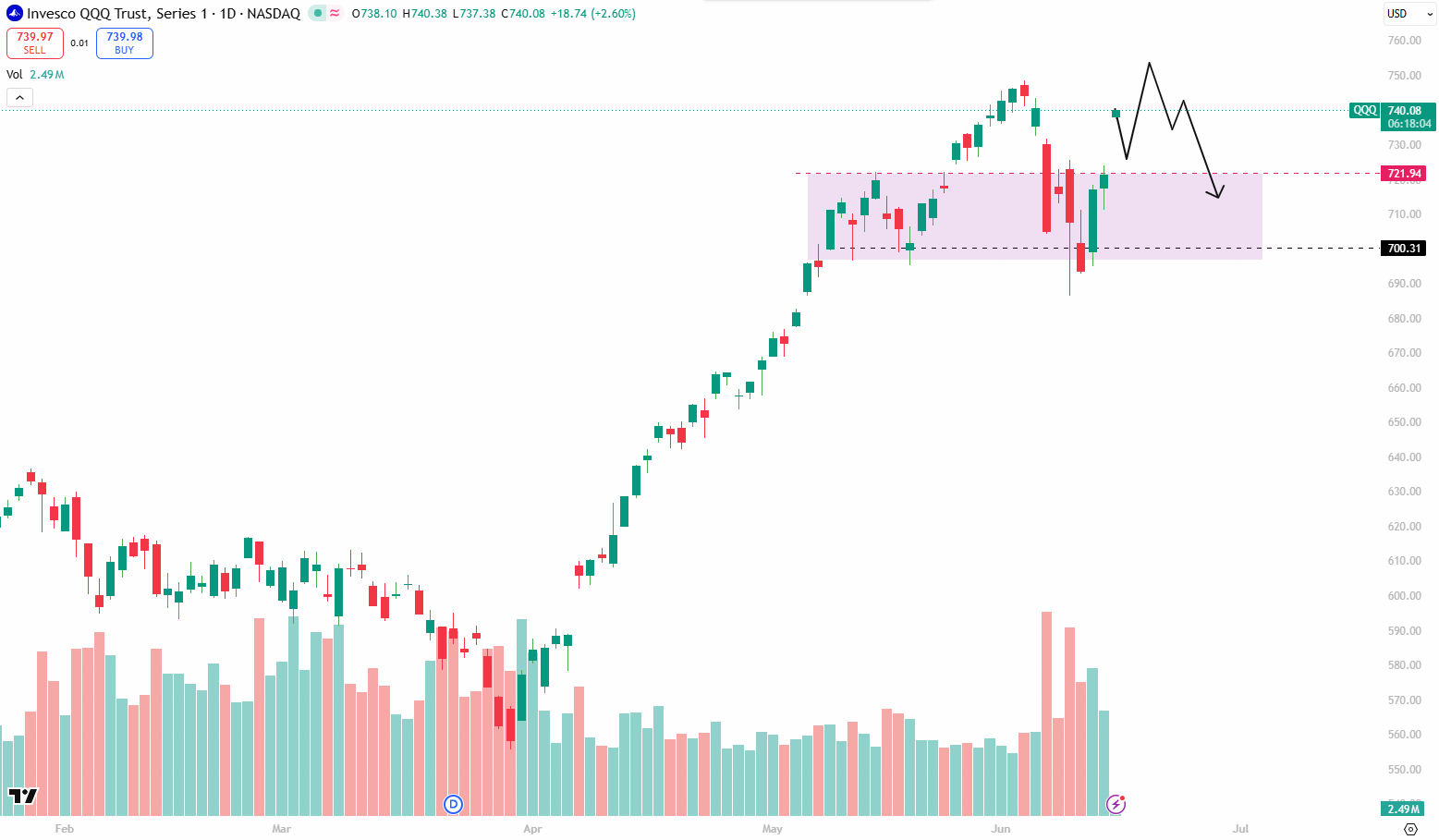

Nasdaq's Big Rally Just Hit a Wall of Indecision - Squeeze Before the Break: QQQ at a Decision Point

- Symmetrical triangle coiling after the big April–June run (610 → 750). Lower highs, higher lows, apex near 720–725.

- Testing the floor. Close 712.60 (-1.73%) sits right on triangle support (708–710). Decision zone.

- Volume = caution. 51M on a red day. Sellers active near the top rail, no demand surge on bounces yet.

- Levels: Resistance 730–735, then 750. Support 708–710, then 685–690.

- Trend intact. 630–640 demand zone is the real invalidation. Above it, this is just consolidation.

- Plan: Break >735 = move toward 750. Break <708 = flush toward 690. Don't chase the middle.

J

Ulta Beauty (NASDAQ: ULTA) — The Beat Nobody Bought: Ulta Is Down 26% After a Strong Quarter

A structurally dominant, high-return beauty retailer is executing well — comps are re-accelerating and management just raised earnings guidance — yet the stock sits roughly 35% below its all-time high. This is the classic "good company, de-rated stock" debate.

Snapshot (as of early July 2026)

| Metric | Value |

|---|---|

| Price | ~$461 (all-time high $706.82 on Feb 17, 2026) |

| Market cap | ~$20B (~44.1M shares outstanding) |

| Year-to-date | Down ~26% |

| Trailing P/E | ~18–20x |

| Forward P/E | ~16x (FY2026 EPS midpoint ~$28.58) |

| EV/EBITDA | ~13.7x |

| ROE / ROIC | ~44% / ~24% |

| Beta | ~0.85 |

| Analyst consensus | Buy — average target ~$627 (range ~$450–735) |

| Dividend | None (initiation under review) |

1. The Fundamentals Are Working

Ulta's Q1 FY2026 print (quarter ended May 2, reported June 2) beat on both the top and bottom line:

- Net sales up 11.1% to $3.16B, with comparable sales up 5.3% — driven by a 3.7% higher average ticket and 1.6% more transactions. Comps came in well above the Street's ~4.6% estimate.

- Operating income up 11.6% to $448.3M; diluted EPS up 15.5% to $7.74 versus roughly $6.86 expected. A sizable beat.

- Gross margin expanded from 39.1% to 40.1%, driven by reduced inventory shrink and better merchandise margins. This matters: the margin gain is execution-driven, not demand-driven, which tends to be more durable.

- $555M returned via buybacks (958,323 shares). Share count is shrinking roughly 5% per year.

- Footprint stood at 1,521 U.S. stores plus 87 international locations, including a presence at the Dubai Mall.

- Inventory rose 12.5% to $2.4B, but almost entirely from the Space NK acquisition, new brands, and 70 net-new stores — inventory per store was up just 1.4%. Clean.

Guidance was raised. Full-year EPS was nudged to $28.36–28.80 (from $28.05–28.55), while sales growth (6–7%) and comparable sales (2.5–3.5%) were left unchanged. The message: management is prioritizing profitable growth over chasing the top line, and is confident enough in profitability to upgrade the earnings outlook.

The growth was broad-based. Fragrance was the strongest category, ticking from 11% to 12% of revenue, and the quarter's TikTok Shop launch plus more than 20 new brands (including Rare Beauty) contributed. Notably, this customer-base expansion is happening without aggressive discounting — TikTok Shop is leaning on curated bundles and exclusives rather than heavy promotion, which protects margin.

2. Valuation: The Cheapest High-Quality Name in Beauty

This is the crux of the case. On a quality-adjusted basis, ULTA is the most attractively priced name in the beauty complex right now.

| Company | Forward P/E | Growth profile | Note |

|---|---|---|---|

| Ulta (ULTA) | ~16x | EPS ~14%/yr, ROE ~45% | Profitable, buyback-heavy, de-rated |

| e.l.f. (ELF) | ~26x+ | Revenue +25%, but FY26 adjusted EPS collapsed to ~$3.13 | High growth, rich multiple, margin compression |

| Estée Lauder (EL) | ~37x (depressed E) | Turnaround, still loss-making (~$930M loss), P/S ~2.9x | "Beauty Reimagined" recovery bet |

| Coty (COTY) | Low, but U.S. business declining ~6% | Structural pressure | Weakest of the group |

| Sephora (LVMH) | Private | Prestige leader | Primary strategic rival |

Ulta's trailing P/E has historically traded in a roughly 12x–20x band. At ~16x forward, it sits in the lower-middle of its own range — cheap relative to its history, and very cheap relative to peer quality: it has the highest ROE, is solidly profitable, and posts positive comps, yet carries the lowest multiple of the group. By contrast, e.l.f. carries a growth premium that looks stretched now that margins have compressed, and Estée Lauder is optically expensive because its earnings are depressed during a turnaround.

The catch: the discount reflects two real overhangs, not just sentiment. It is cheap for a reason — the question is whether that reason is temporary.

3. Strategy: A Barbell Squeeze and One Self-Inflicted Headwind

Ulta operates in a "barbell" competitive environment — Sephora (owned by LVMH) presses from the prestige end, while Amazon and Target press from the mass-market end. Its edge is a mass-to-prestige continuum that no single competitor fully replicates, reinforced by a first-party-data moat built on 44 million-plus loyalty members.

The biggest near-term swing factor is the Target exit. Ulta is winding down its Target shop-in-shop partnership by August 2026 to reclaim brand exclusivity and prioritize its higher-margin standalone model. The move is deliberate and strategically defensible, but it creates a short-term traffic and revenue headwind — and it is a key reason the stock is being discounted.

Offsetting growth levers:

- International optionality. First stores opened in Mexico and the Middle East in 2025, alongside the Space NK (UK prestige) acquisition. Real upside, but with execution, FX, and shrink risk.

- New channels, no discounting. TikTok Shop (reaching Gen Z), a Bath & Body Works partnership across 600+ stores, Uber on-demand delivery, and a Google Cloud–powered AI beauty assistant.

A structural risk to keep front of mind: vendor concentration. Ulta's top 10 partners accounted for roughly 51% of net sales in FY2025. Any major brand shifting its exclusivity elsewhere can leave a mark.

4. The Technical Picture Says the Opposite of the Fundamentals

Here the chart diverges sharply from the earnings story — the downtrend is intact.

- As of mid-June, the price was roughly 13% below its 200-day moving average (~$562), below its 50-day (~$504), with a "death cross" (50-day crossing below the 200-day) formed in May.

- Immediate resistance sits near $543; support near $469. At ~$461, the stock has slipped below that support and is now sitting right on top of its 52-week low near $452.

- The stock is down ~26% year-to-date and ~14% over 90 days — even after beating earnings and raising guidance. That divergence (strong print, weak tape) tells you the market is currently pricing the Target exit and competitive pressure, not the growth beat.

The practical read: fundamentally attractive, technically weak. This is a scale-in on weakness / patient accumulation setup, not a "buy it here" trade. Until the $452–461 support holds and price reclaims the 50-day (~$500+), there is no trend confirmation.

5. Bull vs. Bear at a Glance

Bull case

- Cheap versus its own history and versus peer quality

- Comps re-accelerating; EPS beat plus a guidance raise

- Execution-driven (shrink-led) margin expansion — durable

- ~5%/year buyback shrinking the share count

- International and new-channel optionality

- Unmatched loyalty and first-party-data moat

Bear case

- Target exit is a near-term traffic and revenue hit

- Squeezed from both ends — Sephora in prestige, Amazon/TikTok in mass

- Vendor concentration (top 10 = ~51% of sales)

- Discretionary and macro softness with a value-focused consumer

- Death cross and weak price momentum

- No dividend cushion

Verdict

This is "quality on sale, but the sale has a reason."

On fundamentals, Ulta is the best-run, most-profitable, cheapest-quality name in the beauty complex — 16x forward earnings for a ~45% ROE business with a buyback machine is objectively attractive. But two of the three overhangs, the Target wind-down and the competitive intensity, are real and land in exactly the next two to three quarters, and the chart makes clear the market has not finished discounting them.

My read: watchlist and accumulate on weakness, not chase. The Q2 print (late August) straddles the Target wind-down — that is the real tell. If comps hold near double-digits and margins stay firm as Target rolls off, the thesis is confirmed and the de-rating should reverse. If comps crack, the multiple can still compress toward the low end of its range (~12x, implying a move into the $350s). The risk/reward is attractive, but it demands entry discipline and confirmation at Q2.

A

Market Week Ahead

J

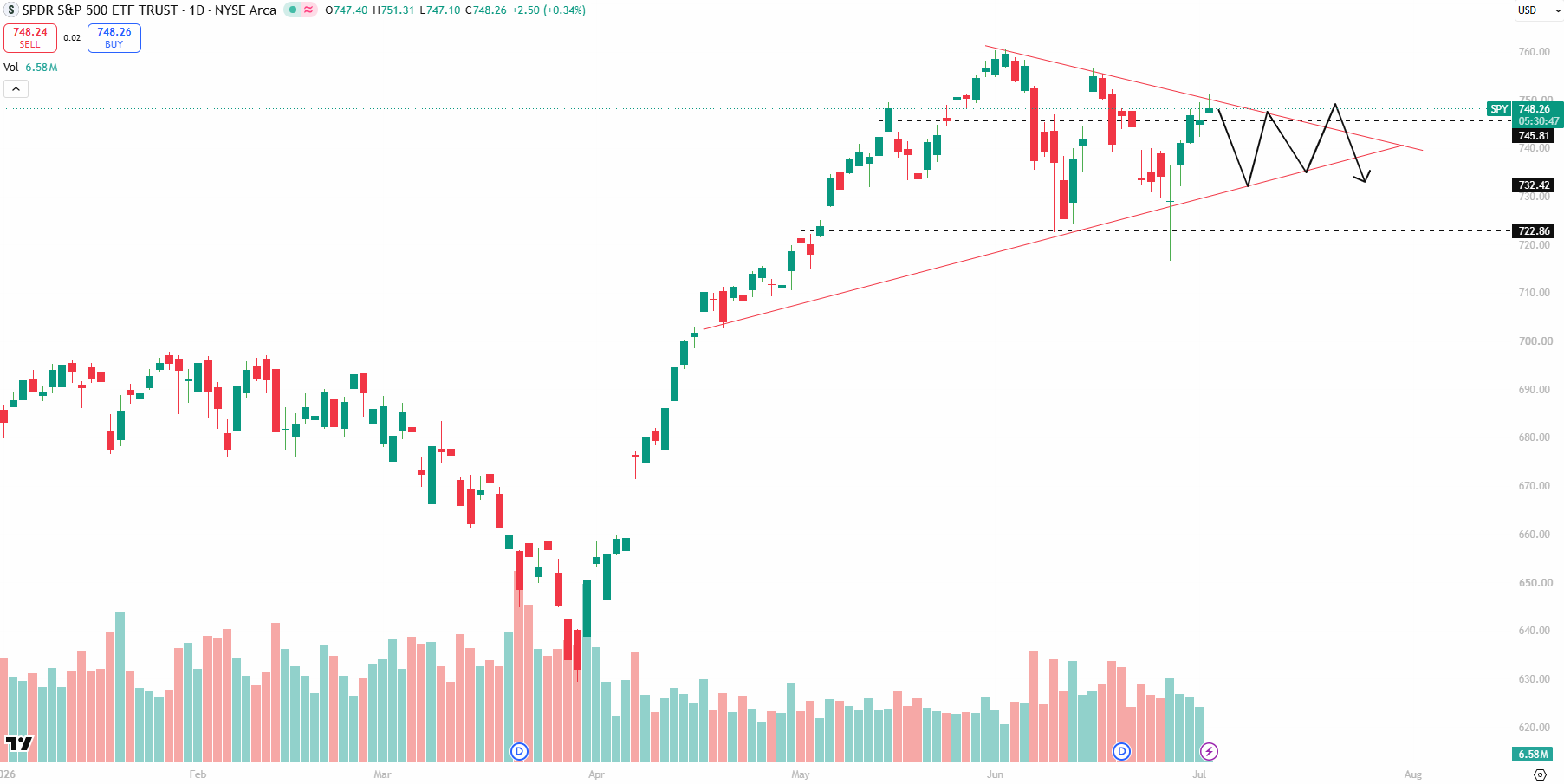

SPY Builds Energy for Next Move After Sideways Consolidation. Downside Move Expected?

- SPY is entering a consolidation phase, trading within a tightening symmetrical triangle after a strong rally.

- Expect sideways price action between 745.8 resistance and 732.4 support until a decisive breakout occurs.

- A fake breakout or fake breakdown is highly possible, creating a liquidity trap before the real directional move begins.

- Avoid chasing the initial breakout. Wait for confirmation or a successful retest to reduce the risk of getting trapped.

- A break below 722.9 would weaken the bullish structure, while holding above it keeps the broader uptrend intact.

- Short-term bias: Neutral/Sideways | Medium-term bias: Bullish unless key support fails.

J

Northrop Grumman (NOC): Down 34% From Its High — Buy the Dip or Falling Knife?

Northrop just fell from an all-time high of ~$765 (March 2026) back down to ~$509. That's a 34% drawdown in a few months. On the weekly chart, price is sitting right on the 200-week moving average — the same trend line that's held for years.

So the question everyone's asking: is this a gift, or a trap?

Here's my honest read after digging through the numbers.

* First, the one-line thesis

Nothing is broken with the business. The stock broke because the mood changed.

That's the whole story in a sentence. Backlog is at a record. Earnings are up big. Guidance was reaffirmed. What actually collapsed was the war premium investors had baked in — and that's a very different thing from a company falling apart.

* What Northrop actually does

Forget the ticker for a second. Northrop is one of the few companies on Earth that builds two of America's three nuclear weapons delivery systems:

- B-21 Raider — the new stealth bomber replacing the B-2

- Sentinel — the new land-based nuclear missile replacing the 50-year-old Minuteman III

On top of that: radars, satellites, electronic warfare, F-35 parts, missiles, and a huge pile of classified work nobody talks about. Four segments, ~$42B in annual revenue.

The reason this matters: the U.S. is spending an estimated ~$95 billion per year for a decade modernizing its nuclear forces. Northrop sits at the center of two of the biggest pieces. That's a demand story measured in decades, not quarters.

* The numbers are good. Genuinely good.

Latest quarter (Q1 2026):

- 💰 Earnings per share jumped 85% to $6.14 (beat expectations)

- 📈 Sales up 4% to $9.9B

- 📦 Backlog: $95.6 billion — a record. That's more than 2 years of revenue already booked.

- Full-year guidance: reaffirmed, not cut

Full-year 2025 was solid too — record backlog, free cash flow up 26%, dividend raised for the 23rd year in a row.

If the business were rotting, you'd see it here. You don't.

* So why did it drop 34%?

Three things stacked up — and notice that none of them are about the actual business:

1. Priced for perfection. After a 60%+ run, NOC needed to crush every number. The quarter was a beat, but full-year guidance only met expectations. For a stock priced that richly, "just fine" was disappointing.

2. A cash-heavy year. 2026 is an "investment year" — Northrop is spending big to expand B-21 production. Higher spending now means lower free cash flow this year (even though it sets up bigger profits later). The market hates waiting.

3. The knockout blow — a peace deal. In June 2026, the U.S. and Iran signed an interim peace deal. Less conflict = less urgency = the whole defense sector sold off together. NOC dropped ~6% in a single session on that news alone.

That third one is the key insight: the stock didn't fall on bad company news. It fell because the world got a little less scary. Those are very different reasons to sell.

* The honest bear case (because I don't do cheerleading)

I'm constructive here, but you should know exactly what you're buying:

- The B-21 has lost money — over $2 billion so far. It's a fixed-price contract on the early jets, so cost overruns come out of Northrop's pocket. There was another $157M hit just last quarter. This program isn't clean yet.

- Sentinel is a budget disaster. The missile program is running 81% over its original cost estimate and is still being restructured, with no locked-in timeline. It's a slow-motion overhang.

- Buybacks got shut off. A January 2026 executive order discouraged defense companies from buying back stock. Buybacks were a big driver of past earnings growth — that lever is now mostly gone.

- 100% dependent on the government. Budget fights, political mood swings, efficiency crackdowns — all real risks when your only customer is Uncle Sam.

- It's fair, not cheap. At ~19–20x forward earnings, NOC trades roughly at its historical average. Lockheed is statistically cheaper. You're not buying a bargain-bin stock — you're buying a quality one at a reasonable price.

* The bull case (why I'm still interested)

- The nuclear modernization supercycle is real and lasts into the 2030s. B-21 + Sentinel = a decade-plus of revenue Northrop has largely locked up.

- Record backlog = visibility. They already have the orders.

- Free cash flow inflects once the heavy B-21 spending winds down — today's pain is tomorrow's cash.

- Golden Dome optionality. 🛡️ Northrop landed a piece of Trump's ~$185B missile-defense initiative. Early days, but it's a brand-new market — pure upside if it works.

- F/A-XX decision coming (~August 2026). Northrop is bidding on the Navy's next-gen fighter. A win would be their first fighter program in 50+ years — and it's basically not priced in.

- Balance sheet is getting stronger. Moody's upgraded the credit rating in late 2025; S&P moved to a positive outlook in 2026.

- Wall Street still likes it. Consensus rating is Buy, average price target sits in the low-$700s — roughly 30%+ above where it trades now.

* 🧭 How I'm approaching it

Not "back up the truck." Not "avoid." Somewhere sensible in between:

- The $500–$520 zone (that 200-week line) is the level that matters. As long as it holds, the long-term uptrend is intact.

- I'd scale in — a starter position here, add more if it defends $509 and reclaims ~$540–$560. Keep some cash back in case it overshoots toward the $450s.

- What would make me more bullish: an F/A-XX win, a Sentinel fix, clean quarters with no new charges, cash flow ramping as guided.

- What would make me back off: a decisive weekly break below ~$490 on heavy volume, a fresh program write-down, or a guidance cut.

* Bottom line

Northrop is a fundamentally strong company with temporarily broken sentiment. The drop was about a fading war premium and a patience-testing spending year — not a company in trouble.

At the 200-week line, the risk/reward tilts favorably if you're patient and can stomach a program hiccup or two along the way. This is a compounder to accumulate on weakness, not a lottery ticket.

J

QQQ at a Critical Level: Sideways Before the Next Big Move?

- QQQ remains in a consolidation phase, trading within a tightening symmetrical triangle after the recent rally.

- Current trading range is 712–736, with price expected to remain range-bound unless either level is decisively broken.

- Bias remains slightly bearish for next week, as lower highs continue to respect the descending trendline.

- This week is likely to stay sideways, with buyers and sellers battling for control inside the narrowing range.

- A breakout above $736 could turn into a bull trap if it lacks strong volume and fails to hold above resistance.

- Wait for confirmation before taking directional positions—a sustained close above 736 would invalidate the short-term bearish view, while a break below 712 could trigger further downside momentum.

A

J

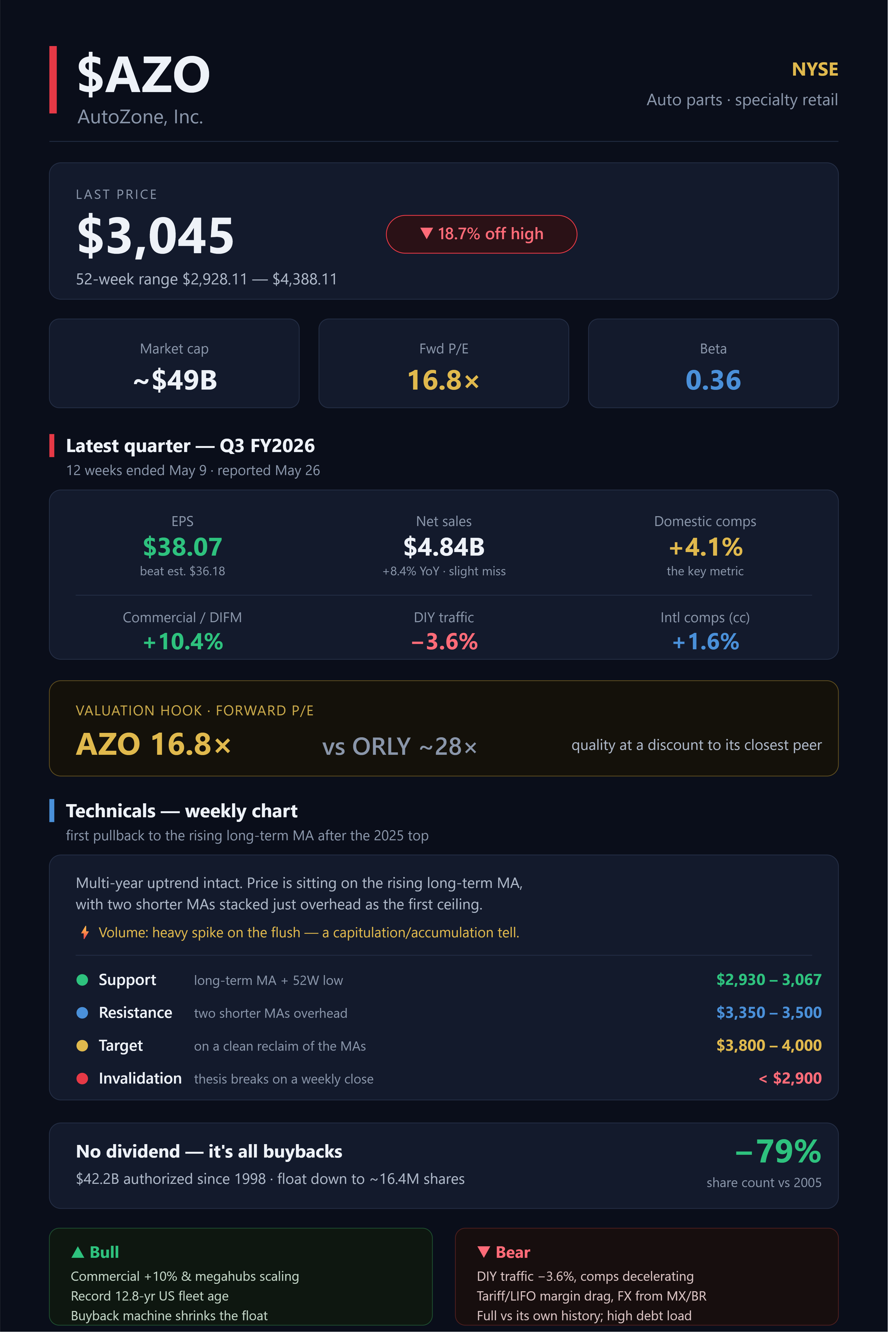

AutoZone, Inc. (NYSE: AZO) - Institutional Data Pull (as of June 24, 2026)

- AutoZone's most recent report is fiscal Q3 FY2026 (12 weeks ended May 9, 2026, reported May 26, 2026): diluted EPS of $38.07 beat consensus of $36.18 by 5.22%, but revenue of $4.84B missed by ~$21.6M (consensus ~$4.86B), and the stock fell 11.41% in pre-market trading on a sharp late-quarter comp deceleration; shares trade near $3,045–$3,054 as of June 23–24, 2026, well below the 52-week high of $4,388.

- The bull case rests on domestic comps of +4.1% (commercial +10.4%, DIY +2.2%), accelerating commercial/megahub momentum, a record 12.8-year average vehicle age, and a relentless buyback ($42.2B authorized cumulatively since 1998); the bear case is decelerating DIY traffic (-3.6%), tariff-driven LIFO charges, soft international constant-currency comps, and a valuation above its historical norm.

- AZO trades at a forward P/E of ~16.8x — a clear discount to O'Reilly (~28x forward) despite comparable quality, a premium to Genuine Parts (~13x), and roughly in line with Advance Auto Parts (~17x). Negative shareholders' equity (-$2.78B) remains by design; Price/Book is not meaningful.

Key Findings

1. Market Data (as of June 23–24, 2026)

- Stock price: ~$3,045–$3,054 (Robinhood quoted $3,054.03 on June 24; Morningstar $3,046.46 on June 23). Note: down ~9% YTD and ~19% off the 52-week high.

- 52-week range: $2,928.11 (low) – $4,388.11 (high).

- Market cap: ~$48.1B–$50.4B (Yahoo/TD Cowen page cited $48.14B on 6/22; public.com $50.45B on 6/3; Morningstar ~$49.7B). Sources disagree by ~5% — verify at publication.

- Shares outstanding: ~16.33M–16.37M (16,369K end of fiscal Q3 per 8-K; Morningstar 16.33M). This is among the lowest absolute share counts of any large-cap, the result of decades of buybacks.

- Enterprise value: ~$60.5B (Yahoo, 6/22/2026).

- Beta: ~0.36 (stockanalysis.com) — low; defensive profile. (Some providers cite higher; verify.)

2. Latest Quarterly Earnings — Fiscal Q3 FY2026 (12 weeks ended May 9, 2026; reported May 26, 2026)

- EPS (diluted): $38.07 vs $36.18 consensus — beat by $1.89 (+5.22%, per Investing.com). Up 7.7% YoY from $35.36. Basic EPS $38.95.

- Net sales: $4,840,950K ($4.84B), +8.4% YoY — the largest growth since Q2 FY2023. Missed consensus (~$4.86B) by ~$21.6M.

- Domestic same-store sales: +4.1% (vs +5.0% in prior-year Q3). This is the key metric. Note: comps decelerated sharply through the quarter — CEO Daniele cited a 5.0% → 4.5% → 2.9% → 1.3% trajectory across the period.

- International same-store sales: +16.6% reported; +1.6% constant currency.

- Total company comps: +5.5% reported; +3.9% constant currency.

- Gross margin: 52.2%, down 57 bps YoY, driven by a 77 bps net non-cash LIFO impact ($20M LIFO charge this year vs $16M credit last year). Ex-LIFO, gross margin was up ~20 bps.

- Operating expenses: 33.1% of sales (vs 33.3% prior year) — leverage from top-line growth.

- Operating profit (EBIT): $923.8M, +6.6%; operating margin north of 19%.

- Net income: $641.5M (vs $608.4M).

- DIY vs Commercial split: Domestic DIY +2.2%; Domestic commercial (DIFM) +10.4% to $1.40B (~34% of domestic auto parts sales). DIY traffic/transactions fell 3.6% — the key soft spot. Avg commercial sales per program per week $18.5 (+4.5%).

- Management commentary:

- Comps/weather: Daniele attributed late-quarter softness to unusually cool, wet May weather, noting on the call that "air conditioning is a great example. it is just been cool in May. Significantly cooler than last year, and it is been relatively wet." He framed it as a timing issue, saying AutoZone is "expecting a normal, if not hotter than normal, summer based on the prognostication of all the weather geniuses out there."

- Commercial: Double-digit commercial growth expected to continue; management says AZO is "under-shared" in commercial (national accounts and up-and-down-the-street).

- International: Mexico and Brazil remained challenged on a constant-currency basis; both consumers described as "under pressure," though AZO believes it is gaining share.

- Inventory: +10.8% YoY (growth initiatives + inflation); net inventory per store -$107K (vs -$142K last year).

- FX: Mexican peso strengthened ~13% YoY, a $74M sales / $20M EBIT / $0.83 EPS tailwind in Q3. CFO Jackson guided to an expected ~$62M revenue / $19M EBIT / $0.78 EPS FX benefit in Q4 at spot rates.

- Q4 LIFO: Jackson guided to a ~$30M Q4 LIFO hit (~45 bps gross margin, ~$1.40 EPS). YTD LIFO charge $177M.

3. Valuation Multiples

- Trailing P/E: ~20.3x (Yahoo, 6/22).

- Forward P/E: ~16.8x (Yahoo 16.81). Note conflict: stockanalysis.com cited 22.10 on an earlier date — likely stale/different EPS basis; ~16.8x is the more current figure.

- EV/EBITDA: ~14.2x (Yahoo); GuruFocus cited ~16.6x; stockanalysis ~17x — sources differ materially.

- Price/Sales: ~2.5x.

- ROIC (adjusted after-tax, non-GAAP): 36.3% for trailing four quarters ended May 9, 2026 (down from 43.5% prior-year period) — still elite, but declining.

- Negative equity (by design): stockholders' deficit -$2,784,552K (-$2.78B) at May 9, 2026 (improved from -$3.97B a year ago and -$3.41B at FY-end Aug 2025). Total debt $9,016,477K ($9.02B). Adjusted debt/EBITDAR 2.5:1. Price/Book not meaningful.

- Cash flow: operating cash flow $847.4M in Q3 ($2.16B YTD 36 weeks); capex $391.7M in Q3 ($1.04B YTD); FY2026 capex plan ~$1.6B (majority to hubs/megahubs), with a similar ~$1.6B planned for FY2027.

4. Analyst Data

- Consensus rating: "Buy"/"Strong Buy." TipRanks: 18 analysts, 15 buy / 3 hold / 0 sell. Other aggregators cite 24–27 analysts; AnaChart cites 58 buy / 5 hold across all ratings.

- Consensus price target (varies by source): ~$3,863 (TipRanks), ~$3,938 (S&P/stockanalysis, 6/4), ~$4,040 (MarketBeat), ~$4,225 (Investing.com, 24 analysts), ~$4,254 (WallStreetZen, 19 analysts). High: ~$4,800 (Raymond James, older). Low: ~$3,200 (Mizuho) / $3,000.

- Recent 2026 rating/PT changes (post-Q3, late May 2026 — virtually all CUT targets):

- Citi: to $3,700 from $4,300, keeps Buy (analyst Steven Zaccone).

- Raymond James: to $4,000 from $4,600, Strong Buy.

- JPMorgan: to $3,850 from $4,300, Overweight (Christopher Horvers).

- BMO Capital: to $4,000 from $4,300, Outperform.

- Guggenheim: to $4,000 from $4,400, Buy.

- Morgan Stanley: to $3,605 from $4,020, Overweight (Simeon Gutman).

- Roth Capital: to $4,023 from $4,526, Buy.

- Mizuho: Hold, $3,200 (David Bellinger).

- TD Cowen: reiterated Buy, $3,700 (June 4, Max Rakhlenko).

5. Peer Comparison — Forward P/E (current data)

| Ticker | Price | Market Cap | Forward P/E | Notes |

|---|---|---|---|---|

| AZO | ~$3,045 | ~$48–50B | ~16.8x | Trailing ~20.3x |

| ORLY | ~$85.63 (6/22) | — | ~28.4x | THE key comp; trailing ~30.8x; post 15-for-1 split (June 2025); most expensive in group |

| GPC | $106.47 (6/23) | $14.65B | ~13.3x | Spinning off into two companies; trailing P/E (~245x) distorted by charges |

| AAP | $54.81 (6/23) | $3.31B | ~17.2x | Mid-turnaround; trailing ~49x |

| MNRO | ~$15.58 (6/18) | ~$467M | disputed: ~26.5x (StockStory) vs ~46.9x (stockanalysis) | Turnaround, near-zero earnings; trailing P/E (~570x) not meaningful |

- Takeaway: AZO trades at a meaningful discount to O'Reilly (~16.8x vs ~28x) despite comparable best-in-class quality, supply chain, and buyback discipline — the central valuation hook. It carries a premium to GPC (~13x, but GPC is mid-restructuring/spin-off) and is roughly in line with AAP. ORLY's premium reflects its longer comp track record (33 consecutive years of comp growth) and higher commercial mix.

6. Business Segment Detail

- Total stores: 7,856 as of May 9, 2026 — 6,766 US, 933 Mexico, 157 Brazil. Opened 82 net new stores in Q3 (57 US, 20 Mexico, 5 Brazil); FY2026 plan ~355–365 stores.

- Megahubs: CFO Jamere Jackson said on the Q3 call that AZO opened 14 megahubs in the quarter for a total of 156, with plans to open 15 more in Q4 and a long-term target of ~300 at full buildout (at least 40 planned in FY2027). Megahubs carry 100,000+ SKUs in ~33,000–35,000 sq ft and serve as fulfillment points for surrounding satellite stores; many are repurposed big-box vacancies (former Kmart, Toys R Us, Bed Bath & Beyond, Big Lots). Caveat: earlier FY2026 sources cited 137 megahubs (Q1) and a "200+" near-term target — the count has ramped over the year and "200+" vs "300" framing has varied; 156 is the most recent figure.

- Duralast: private-label parts brand (duralastparts.com) — key margin and differentiation driver.

- ALLDATA: automotive diagnostic, repair, collision and shop management software (alldata.com). AZO derives no revenue from repair/installation services.

- International: Mexico 933 stores, Brazil 157; accelerating openings, targeting up to ~500 annual store openings by 2028. Management is "bullish on international being an attractive and meaningful contributor."

- Management (confirmed current): CEO Philip B. Daniele III (named President & CEO January 2, 2024); CFO Jamere Jackson (CFO since January 2021, EVP Finance & Store Development; former Hertz and Nielsen CFO). COO Tom Newbern. Capital-allocation philosophy: "disciplined approach of increasing earnings and cash flows to drive shareholder value," maintaining investment-grade credit ratings and targeting adjusted debt/EBITDAR ~2.5x.

7. Capital Return

- NO dividend.

- Q3 FY2026 buyback: repurchased 164K shares at avg $3,582, total $586.3M.

- Authorization: $804.2M ($0.8B) remaining at end of Q3; on June 16, 2026, the board authorized an additional $1.5B. Per AutoZone's 8-K, "Since the inception of the repurchase program in 1998, and including the above amount, AutoZone's Board of Directors has authorized $42.2 billion in share repurchases" (CFO Jamere Jackson).

- Cumulative repurchases since fiscal 1998: $39.85B / 155,985K shares (at ~May 2026).

- Multi-decade share-count reduction: from ~77.3M shares (May 2005) to ~16.37M now — and AZO has bought back more than 100% of its then-outstanding 1998 share base, at roughly an 8.2% average annual reduction. (Jim Cramer characterization: from ~31M a decade ago to <17M today, ~87% reduction since IPO.)

- Sustainability: funded by FCF plus incremental debt while targeting adjusted debt/EBITDAR 2.5x and investment-grade ratings. Negative equity is a deliberate output of this model, not distress; analysts nonetheless flag the leverage and the declining ROIC (36.3% vs 43.5%) as risks if FCF growth slows.

8. Sector Backdrop

- Average US vehicle age: 12.8 years in 2025 (S&P Global Mobility) — a record and the 8th consecutive annual increase (passenger cars 14.5 yrs; light trucks 11.9 yrs). 289M light vehicles in operation (+3M YoY); 4.5% scrappage rate. Aftermarket lead Todd Campau: "The vehicle fleet continues to demonstrate impressive resilience even as it faces stress from high new and used prices and economic uncertainty." The 2015–2019 heavy-registration cohort is now entering the prime 6–14-year repair window — a structural aftermarket tailwind. (This is the latest published S&P figure; the next annual update typically lands in spring/summer.)

- Miles driven: US VMT at/near record highs (FHWA data through April 2026); FHWA long-term forecast ~+0.6%/yr through 2053. Supports parts wear/demand.

- New/used affordability: Prices elevated, partly tariff-driven; one estimate puts Q1 2026 average new-vehicle prices $8,000–12,000 above Q4 2024 (tariff component ~$4,000–6,000). High prices push consumers to keep and repair existing vehicles — favorable for AZO.